Stablecoins can work for cross-border

Compliance may be the challenge

Reader note: Payments in Full will not become a Stablecoin Substack, but this week is again about Stablecoins and next week I will post on the GENIUS Act. After that, I will pivot back to incumbent methods.

Key insights in this post

My recent post on Stablecoins drew the conclusion that they were not that useful for domestic commerce but, might hold promise in cross-border use cases

This post concludes they indeed improve cross-border money movement in some uses cases, particularly were the destination involves an “exotic” currency

Retail:

Transfers:

Fintechs like Wise have already driven down prices and made 60%+ of transfers near instant; they do this by leveraging local instant systems; Stablecoins can’t improve this too much

Stablecoins transfer the FX risk to the receiver who may not be in a position to get the best rate, so E2E cost may be higher

Stablecoins have an advantage in exotic currencies where there is no instant system and the receiver may prefer to keep their value in dollars

Commerce

Stablecoins are only faster than cards until if the recipient doesn’t convert to fiat

Card networks offer a mid-market FX rate, which is competitive

Card networks have layered on cross-border surcharges than make them less cost competitive, but they could unwind those fees if Stablecoins take share

Safety & Compliance:

Stablecoin blockchains are as safe or safer than incumbents, but both systems are vulnerable via their connective systems and to scams

Compliance is not inherently different in either model, but Stablecoin Issuers are less mature in their processes

Stablecoins have immature chargeback processes if consumers have a legitimate dispute with the merchant

Stablecoins are clearly superior if the receiver want to keep their value in USD

Wholesale:

Speed & Cost:

Cross-border wholesale payments markets are so concentrated in developed economies and mega-banks that Stablecoins do not provide a cost advantage and may not even be faster to get to fiat

Outside major markets, Stablecoins are meaningfully faster and lower friction than SWIFT/Correspondent banking; they are also better where USD is the preferred unit of account. In these cases, keeping currency in USD is a feature, not a bug.

Safety: Stablecoins blockchains are as safe or safer than incumbent systems, but both systems are vulnerable via their connective systems and to scams

Compliance:

Not inherently superior in either model, but Stablecoin Issuers are less mature in their processes

Stablecoins & Crypto have been used to avoid national currency controls because the money doesn’t actually cross a border until converted to fiat

Smart Contracts may be particularly valuable in Trade Services where transactions like Documentary Collections already operate on a similar model. This could be a good entry point for stablecoins.

Conclusion: Stable coins have real advantages in some cross-border retail & wholesale use cases, but they are not everywhere and always the best choice

Introduction

In a prior post, I found limited utility for Stablecoins in domestic commerce: Stablecoins were not really faster, cheaper, or safer than incumbent payment methods when viewed from an end-to-end perspective; they also faced a compliance challenge.

I promised to address Stablecoins cross-border utility in a future post. This is that post. I take this on with some trepidation. I haven’t had as much experience in global payments as in domestic, and the experience I have is more retail-focused. Stablecoins have retail use cases in remittances, but are more interesting in higher value payments where my knowledge is weaker. Forgive me my errors in advance.

That prior post described my views as “pro-stablecoin, but “anti-hype”. There is lots of hype around cross-border stablecoins, but some of it is justified. It actually is a better mousetrap than incumbent methods for certain use cases. As we shall see, the biggest challenge will be whether those technical advantages survive the compliance thicket.

Retail

Retail cross-border transfers have improved over the last ~10 years or so as digital services displaced in-person services. Stablecoins don’t improve the situation too much except in “exotic” currencies. For commerce, they are definitely less expensive due to Card Network pricing, but lack robust chargeback processes.

Transfers use case

In transfers, Stablecoins are competing more with Fintech solutions than with bank solutions. The Fintechs have addressed many of the friction points except in Exotic currencies.

Faster

Fintech methods for cross-border retail transfers can settle quickly. Increasingly, providers like Wise use Instant Payment rails at both ends of the transaction such that E2E settlement can be close to real-time. Wise claims 60%+ of its transactions are effectively instant. More exotic currencies and less-developed markets take longer. The roll-out of new instant rails to new countries will drive this percent higher in the years to come.

Money is moving between accounts maintained by the Fintech at both ends and does not need to traverse correspondent banks individually. Effectively, it is an intracompany book transfer. To accomplish this, the transfer company needs to maintain liquidity in every country to fund the expected flows. It then settles among its own accounts to ensure liquidity for the next round. Those settlement transactions do traverse the correspondent system.

This analysis applies primarily to countries with developed banking systems, local instant rails and banked consumers. For cash transactions, the money moves cross-border just as fast, but money-in/money-out processes are still manual. Yet, even these transactions can be same day.

For now, Stablecoins have faster availability only in markets that don’t have instant rails. But stable-coin settlement is only instant if the money doesn’t need to move to local currency. Stablecoin redemptions may move via ACH which has overnight settlement.

Cheaper

Some banks offer retail transfers, but most do not do so at scale; incumbents are mostly in-person services like Western Union or digital Fintechs like Wise & Remitly. The in-person providers have digital services as well.

Historically, in-person remittances have been expensive for low value transfers. Senders often pay a high fixed fee and a high FX spread. Many transfer companies inflate the exchange rate as it is hard for a retail customer to benchmark.

This has changed due to competition from digital services who offer more modest fees and whose FX rates are pegged to an external benchmark. Wise for example has a transparent pricing model:

Fees: A flat fee plus <100bps of value

FX: The “Mid-market” FX rate benchmark

Exception costs: For example, if the transaction uses SWIFT or a Correspondent there are additional fees

Stablecoins change this equation.

“Gas” fees can be de minimis for retail transfers. Some providers charge off-ramp fees to move the money back to fiat

FX is subject to competitive bidding at the receive end, in theory

In incumbent methods, the sending service usually charges the sender for FX at a captive rate. The sender must change providers to get a better rate which may be offset by higher fees

In Stablecoins, FX is converted at the receiving end and, in theory, rates are subject to competition. In practice, few FX providers compete yet

Stablecoins effectively transfer FX risk from the send side to the receive side. The receiver has to transfer to fiat and bear the FX spread and any off-ramp fees. Given the receiver is usually the less affluent and sophisticated of the counterparties, this isn’t ideal.

Safety & Compliance

Compared to the Fintech solutions, Stablecoins offer no inherent advantages or disadvantages on safety and compliance. The underlying networks are secure, but subject to scams just like all other payment systems. They both improve on the physical safety of the receiver since neither requires in-person acceptance of currency.

Commerce use case

Stablecoins are substantially less expensive than cards but lack some of the consumer protections of the card system.

Faster — Just as in domestic payments, stablecoins can clear faster in USD, but take just as long to clear in fiat — which is what merchants want. If the merchant wants to keep their proceeds in USD, stablecoins are indeed faster.

Cheaper — The incumbents are cards, usually credit cards. The cost to the receiving merchant includes standard interchange, cross-border surcharges, and FX spreads. Settlement currency can also impact the rate.

Network FX rates are generally similar to Wise’s mid-market rate. In the Stablecoin case, the merchant (receiver) needs to convert from dollars to local fiat, which may go through their own bank at a high spread or might be available through a blockchain exchange at a lower spread. Such exchanges are still nascent and may not yet be competitive.

Interchange, network fees, and cross-border surcharges can consume 1-3% of face value compared to the Stablecoin Gas Fee which might but under a penny. This is a material difference, particularly since the Stablecoins are irrevocable. The card networks could remain competitive by cutting those fees, but since cross-border generates about one-third of their revenue, that would be painful to their shareholders. Merchants are the big winners here.

Safer — For retail commerce the safety difference is not apparent.

Both systems are secure at the network level

The surround systems may be vulnerable to cybercrime in both models

Both systems are vulnerable to social engineering (scams) and 2nd-party fraud

For routine chargebacks, the card system has well developed processes while in Stablecoins the consumer (buyer) is at the mercy of the seller (merchant). This is the same issue we encountered in the domestic use case. Merchants like that Stablecoins are irrevocable, but that is not in the consumer’s interest

Compliant — All cross-border money transfer systems have to address global AML/KYC compliance and local regulations like capital controls.

AML/KYC — These are global rules that apply on both the send and receive side of a transfer. Generally, account-to-account transfers between major banks in leading economies can do this relatively easily. Banks need to do KYC to open an account and they need to monitor all transactions for suspicious activity. Fintechs need to so this de novo, without seeing the broader picture of a customer’s transactions. Given most money transfer Fintechs are globe-spanning but modest in size, this remains a challenge. Stablecoin issuers face the same scale challenges

Local regulations — This is the key challenge in many developing countries. They may have capital controls in place or other kinds of restrictions to address money laundering, tax avoidance, etc. Stablecoins aren’t really in-country until they are converted to fiat and they can’t be controlled through the banks that operate under local licenses. They just exist on the internet as entries on a blockchain.

In developed economies regulations are evolving to bring Stablecoins into the mainstream, e.g., the GENIUS Act. In developing economies, one of the appeals of Stablecoins is that they are outside the control of the local government. In some ways they are back-door “dollarization”. My sympathies lies with the consumers here, but the law is the law.

Once the Stablecoin converts to fiat, the funds are within the conventional banking system where local regulations are enforced. The tipping point is the off-ramp. But if the consumer wants to keep their cash in dollars they don’t need to off-ramp.

Conclusions on Retail

In Retail, Stablecoins improve cross-border commerce more than cross-border transfers, but they have advantages in both use cases:

To summarize,

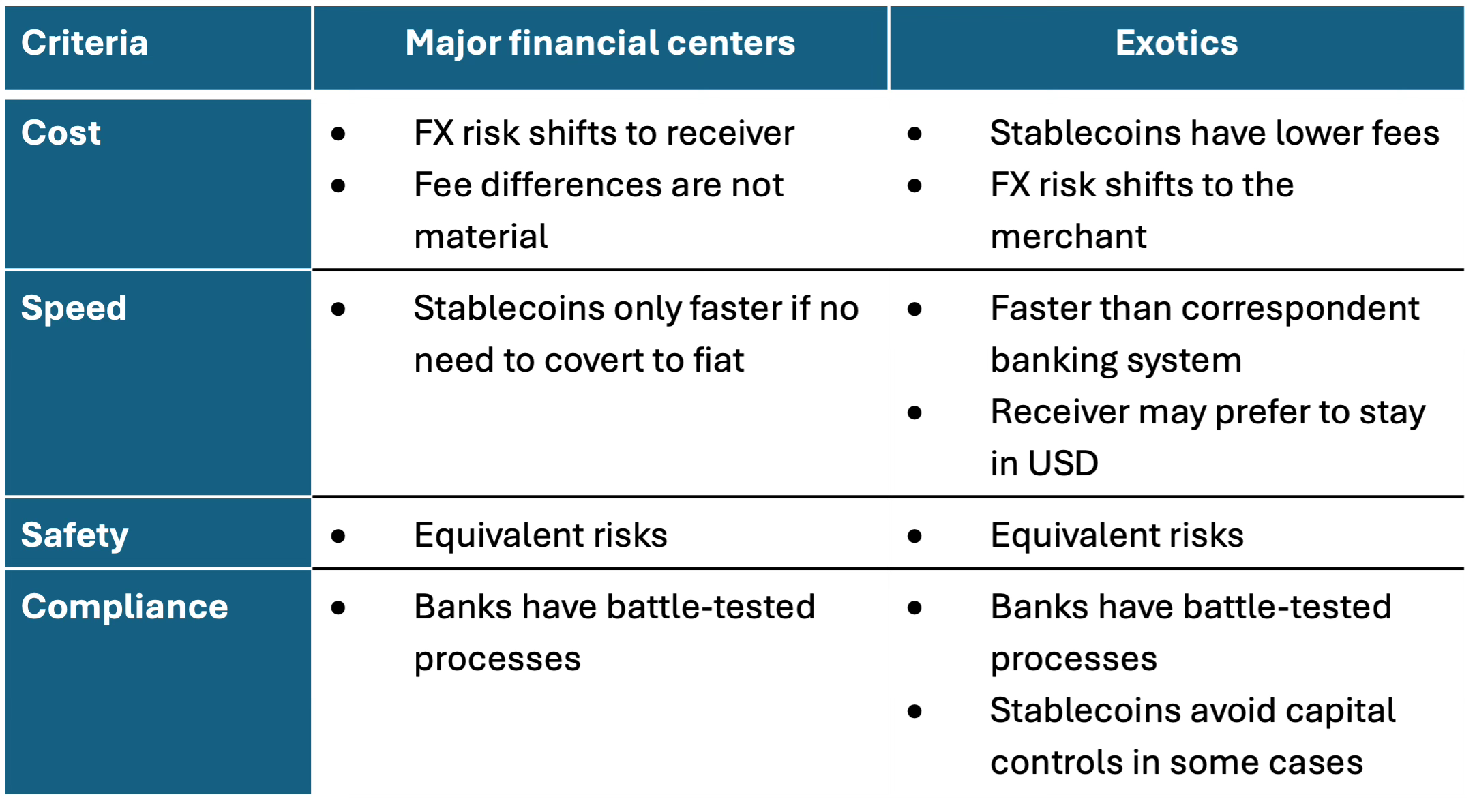

For Transfers: Stablecoins beat incumbent methods on cost and speed in exotic markets but FX risk transfers to the receiver. In developed markets, they are roughly equivalent to digital fintech transfers

For Commerce: Stablecoins are less expensive than cards due to network cross-border surcharges. They are roughly equivalent in speed to fiat

Stablecoins could represent some compliance risk due to their immaturity, but there is nothing inherently non-compliant about the technology. Stablecoin issuers face the same challenges as incumbents: they are global in scope but limited in resources. Most of the biggest providers have brought senior ex-regulators onto their boards and management teams to address this. But compliance adds friction which may slow down transactions and add cost. Someone has to pay for all that, because the compliance standard is the same regardless of the technology used.

Wholesale

Wholesale transfers are more complicated than retail. Volume is concentrated among the biggest banks in the biggest financial centers. Flows around capital markets dwarf flows around trade. Within Trade, a considerable share (~30%?) is intra-company; for example, Apple US importing iPhones from its Chinese factories or paying out royalties to its Irish subsidiaries that own the IP. That trade is completed by book transfers between related entities.

For the trade that is inter-company and not for capital markets, companies use a combination of SWIFT messaging and foreign wire transfers.

SWIFT a utility “for transmitting payment instructions and other financial messages between banks and other financial institutions. SWIFT itself does not hold funds or process transactions; it simply provides the messaging infrastructure”

Cross-border transfers can either traverse a single bank with branches in both endpoints or use a “correspondent” bank in the destination market. If the destination market is an “exotic” currency, more than one correspondent may be required. Adding correspondents increases costs and settlement times

So SWIFT transfers information while the correspondent system moves money. In Stablecoins, both functions are handled by the blockchain. The SWIFT/ Correspondent system relies on closed networks while the blockchain uses the public internet, secured by cryptography.

How do the two systems compare on Speed, Cost, Safety, & Compliance?

Speed & Cost

The FX markets are heavily concentrated in the top 10 providers, who therefore can deliver the lowest rates. Those same providers typically have the broadest footprints and the highest scale. Transactions between major providers in major financial centers move faster than elsewhere – and those kinds of transactions dominate cross-border trade – approximately two-thirds of trade is among developed countries. The financial flows would follow.

That doesn’t mean Stablecoins can’t improve speed somewhat within that two-thirds, but Stablecoins have bigger advantages outside those developed markets. Further, in developed markets, counterparties are more likely to convert the Stablecoin from USD to local currency (e.g., Euro, Yen, Sterling, etc) and move it to a bank whereas in developing countries, leaving it in a USD Stablecoin might be preferred.

As one example, most of the Oil trade is done in USD; so, having a lower-friction version of USD in Stablecoin form might improve market efficiency. Many other commodities are also USD-centric.

Stablecoins also have the advantage that data and payment are in the same transaction message and not split between SWIFT and the Correspondent system. SWIFT fees are marginal to transfer economics but having to associate the SWIFT transactions back to the funds transfer adds friction. Major banks and corporations have this automated of course, but not every bank or corporation is major – particularly in developing markets.

To summarize for wholesale, outside major markets, Stablecoins are meaningfully faster and lower friction than SWIFT/Correspondent banking; they are also better where USD is the preferred unit of account. In these cases, keeping currency in USD is a feature, not a bug.

In developed markets, Stablecoin is faster in USD, but still needs to convert to local currency using a local payment method, which adds a delay and may impact the FX rate. Further, most conventional transfers among financial centers move faster than the average — the performance gap is narrower.

Safety

The risks in both systems are not with the underlying networks but with the surround systems. The famous “Bangladesh Bank cyber heist” from 2016 ultimately cost as much as $100M. The heist was executed using SWIFT messages but the error was not on SWIFT itself, but in a Bangladeshi bank that was connected to SWIFT. Most major crypto companies have seen cybercrime executed via the blockchain without the blockchain itself being hacked – the flaw was in the attached systems.

Global banks monitor transfers for cybercrime. For example, some corporations have imperfect controls around transfers which an insider or cybercriminal might exploit. The bank’s systems can detect out of pattern transactions to new counterparties and alert their client’s management before sending the money. The crimes occur outside the payment system, on the corporate side, so Stablecoins will face the same challenges. Note that the Bangladeshi incident was discovered by the Fed when a person noticed misspellings in a SWIFT message.

I think it is fair to say that both networks are secure, but they rely on the sender and receiver systems to monitor for fraud and abuse, not the network itself.

Compliance

Compliance could upset the applecart. Stablecoin providers are vocal about their efforts to be compliant. They invest in KYC and AML monitoring systems and have made major strides since the earlier, wild west days of Crypto.

But there are a few compliance issues where pretty good may not be good enough: “Know your counterparty” & national capital controls.

Know your counterparty

Regulators expect transfer providers not only to verify the identity of their own customer (KYC) but to ensure that the money is sent to a legitimate counterparty. This is sometimes called “Know your customer’s customer”.

This includes topics like sanctions screening, OFAC compliance, PEP analysis and other obscure terms that ensure funds are not going to a nogoodnik. Often what slows down the correspondent system is not technology, but the inability to verify the identify of the counterparty to the sender bank’s satisfaction.

JPMorgan even developed a blockchain-based system called LIINK to exchange such compliance data efficiently between banks. Only banks and payments Fintechs are allowed to use the system. Like SWIFT, LIINK moves data not money, but it expedites payments by resolving correctable compliance data.

One of the reasons the correspondent system can be slow in exotic markets is that regulators have pressured banks to trim their correspondent networks to ensure the entire network is sound on AML. That means more “hops” between banks to get money to its end destination. It is also harder to verify identity in those markets.

It is not clear to me how Stablecoin issuers can address this topic. They may rely on the off-ramp banks or they may build some of the functions in-house. This function is hard to automate.

Capital Controls & Dollarization

To be clear, I am way out over my skis on this topic. It is a common enough discussion area in the Stablecoin world so do your own research rather than just relying on me! But here we go.

What the private sector views as a feature of Stablecoins, some governments might view as a bug. In the correspondent model, money is either in-country or off-shore. For in-country funds, governments can regulate exchange rates, limit outflows, etc.

With Stablecoins, money isn’t in-country until the owner redeems it into a bank account. Stablecoins exist on the internet which knows no borders. A supplier can still be paid for an export but the money stays out of the country, in a USD-denominated Stablecoin. That supplier can then use the Stablecoin to buy supplies it needs to import for the next round of manufacturing. This is particularly important if the home country has high inflation or a volatile currency.

But the more that local industry relies on Stablecoins for trade, the less control the local government has over economic policy. Stablecoins effectively push local currency into narrower niches. This is known as Thier’s law where “good money drives out bad money”. This phenomenon happens with physical money as well. In hyper-inflating countries, dollars often circulate locally. Famously, Kent cigarettes had this role in communist Romania. Bitcoin and other Crypto currencies serve a similar role when countries have a currency crisis. You can sympathize with the citizenry while acknowledging that it may be locally illegal.

Stablecoins for trade services

As I discussed in my domestic post, Stablecoins have an advantage in Smart Contracts and Micropayments. Smart contracts are more relevant to this discussion as some Foreign Trade operates in ways very well suited to smart contracts.

Both Letters of Credit and Documentary Collections require a bank on the import side to validate documentation to trigger a release of payment. Payment isn’t guaranteed, but the validation triggers the obligation to pay. The bank plays the “Oracle” role I discussed in my prior post. Today, these services are full of friction. Smart contracts can grease the wheels in the end-to-end transaction.

Conclusions on Wholesale

What I draw from this analysis is that Stablecoins don’t create enough incremental value in Financial Centers to displace incumbent methods. The incumbents are inexpensive enough on fees and provide the best FX rates. The system is fast enough for regular trading partners in major markets. But Stablecoins may be a better mousetrap in exotics where the Correspondent system is slow and expensive. It is also better in commodities trading where the dollar is already the unit of account.

If Stablecoins can develop more use cases for Smart Contracts, they could gain traction even in the financial centers.

Conclusions

Stablecoins have real advantages in some cross-border retail & wholesale use cases, but they are not everywhere and always the best choice:

They have more value in Exotic currencies and markets than in developed markets

They typically migrate FX risk from the sender to the receiver which may not always be preferred. If non-USD coins gain scale, this problem goes away

They are faster only where the receiver wants to keep their money in USD. If the receivers want local currency there is a delay

They face the same compliance challenges as the incumbents but need to comply from a lower scale position

Overall, Stablecoins are a more efficient way to move money across borders. In the short run, they will be applied where the inefficiencies of the current system are most apparent, i.e, exotics. From there, they may migrate up-market as scale builds.

Their biggest obstacle is the ability to do rigorous compliance in an area where regulators are very strict. Welcome to the club!