Klarna Klunks

Fewer polemics, but also less clarity

Key insights in this post

Klarna Q4 earnings release was not well-received by investors, with the stock falling 25% immediately after and a total of 50%+ YTD

The story they are telling is that the new growth engine is Fair Financing (FF), a longer-term installment loan similar to Affirm’s primary offering

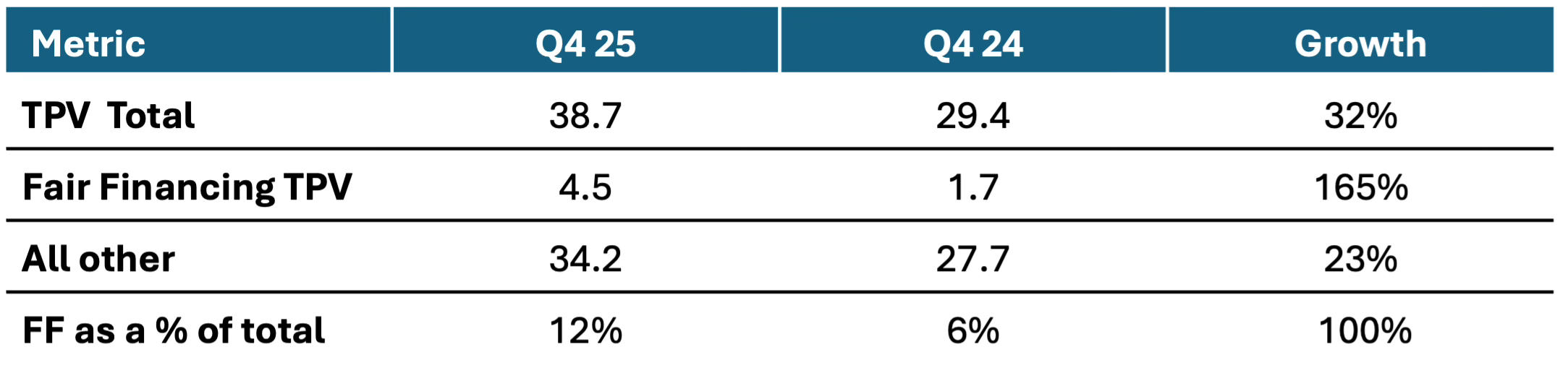

FF grew TPV 165% vs. 23% for all other Klarna products

FF grew from 6% to 12% of TPV YoY

Klarna’s reported metrics do not give a clear picture of their financial situation, particularly if more of its volume will be longer-term Fair Financing loans

They focus Unit Economics on Revenue growth of 25% rather than Transaction Margin growth of 2%. Transaction Margin is the better measure of unit economics

They measure credit costs as a percent of GMV (a.k.a. TPV) rather than outstanding loans. This understates credit costs because 37% of TPV is not lending

They have high funding costs that they are addressing through securitization and a US bank charter

Securitization is effective, but trades long-term revenue for short term gains

A US bank charter is unlikely to lower funding costs as other Fintech lenders with charters show

Klarna’s proposed transaction account offerings do not align with its borrowers demographics and are unlikely to gain traction

Overall, Klarna did not provide comfort that they can just grow their way out of their challenges

Introduction

Klarna published Q4 earnings with a thud. Almost mirroring PayPal’s fall, Klarna’s stock is down 50% for the year with about a third of that drop happening after Q4 earnings. As they emphasized, revenue growth was robust, but they missed a few metrics and 2026 guidance was disappointing. That makes the stock drop about missed expectations rather than actual results.

They lost $273M for the year. In fairness, most of that loss was from earlier in the year with only $26M happening in Q4. However, they earned $21M in 2024. In the bad old days of 2023, they lost a similar $244M on much lower volume.

Good luck finding any net income figures in the “Investor Presentation”, which is where I went first. Instead, you need to read the “Earnings Release” or the “Historical Financial Statements” to find any mention of Net Income.

These reports scaled back from the optimistic and colorful Investor Presentation Klarna published for Q3 earnings. The materials were noticeably missing most of the polemics about incumbents as well. In general, a business-like set of materials.

Klarna made a clear pivot from Pay-in-4 being the hero product, to Fair Financing (FF) being the hero. That shift is reflected in the results and might call for reporting changes for future periods. The higher the share of Fair Financing that Klarna books, the less helpful some of their preferred metrics are for describing the business.

That will be the focus of this post.

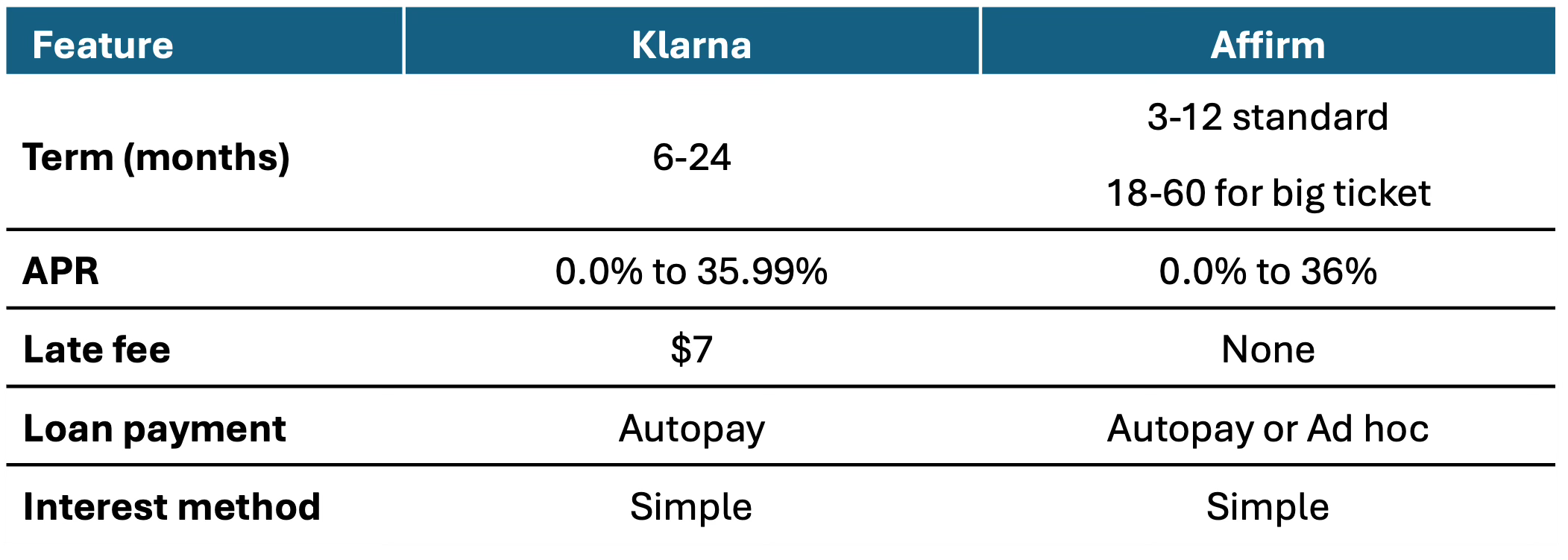

Fair Financing is more conventional than Pay-in-4

Fair Financing is a conventional installment loan with a few quirks. It closely compares to Affirm’s standard installment loans:

While the APRs are identical, the 0.0% APR option may be different. Affirm offers 0% when a merchant agrees to subsidize the interest. Their Peleton arrangement originally worked like that. High interest rates mostly killed that off, but it has been rising again according to Affirm’s disclosures: About 16% of loans are 0% APR growing at 65% YoY.

In contrast, Klarna’s disclosures don’t mention a merchant subsidy. The FF 0% seems to be awarded at Klarna’s discretion based on term, credit risk, ticket size and other criteria. Since it is discretionary, I suspect few customers qualify.

Both lenders require repayment via debit or ACH, but Affirm allows the payment to be client-initiated rather than autopay. Klarna does not seem to offer that option. In fact, the Klarna late fee only kicks in after Klarna itself has tried to debit the borrowers bank account twice without success. $7 is low for a late fee, although not as low as Affirm’s $0. Klarna caps the fee at 25% of ticket value.

How big is Fair Financing?

Klarna made some new disclosures on Fair Financing TPV and growth rates.

For comparison, 83% of Affirm’s transactions compare to Fair Financing. They had approximately $36B of installment TPV growing at 28%. Affirm added 2x as much volume in its last year.

Fair Financing grew at very high rates, but other products grew at “only” 23%. The “All Other” category includes Pay-in-four, Klarna Card, Pay-in-full, and a few other items. Some of these were broken out to a degree in the Q3 release, but not disaggregated here. For comparison Affirm’s Pay-in-X product grew at 55% last year, albeit from a much lower base.

Pay in Full was shown as 20% of Klarna TPV as of Q3. Assuming it is still that high in Q4, then 68% of TPV is likely Pay-in-4. FF loans are larger, so a given TPV supports fewer loans. As a result, the operating costs to support FF should be lower share of total cost.

Klarna did not give abandon anti-incumbent polemics entirely. The Earnings Release makes the following statement:

“Traditional banking monetizes misery through revolving debt. We’re building a global digital bank that saves consumers time and money and puts them in control of their finances.”

Klarna had a case on Pay-in-4 since those are 0% APR, short-term loans. But Fair Financing has APRs as high or higher than Credit Cards, longer terms, and late fees. The consumer has to apply for an FF loan each time, so it takes more of consumer’s time than a Card.

Klarna itself encourages repeat use via the Klarna Card, which now accounts for 15% of transactions. I fail to see how taking a series of FF loans is better for the consumer than spending on a standard credit card. Klarna Card TPV grew at 209% in Q4 YoY. So Klarna itself is encouraging its customers to spend and borrow.

As for control, it depends on how many loans Klarna makes to its customers. Most major US card issuers now let consumers structure their repayments as installments, so they help customers stay as disciplined as they are on Fair Financing. If borrowers are undisciplined and Klarna is a liberal lender, debt traps are not avoided, just fragmented across several loans.

Klarna should not be making statements like this if it is going to ride Fair Financing as its marquee product going forward.

What metrics are at issue?

I pointed some of this out in my post on Q3 Earnings, but the differences are more stark now that Fair Financing is the growth engine:

Focus on Revenue rather than Net Interest Margin

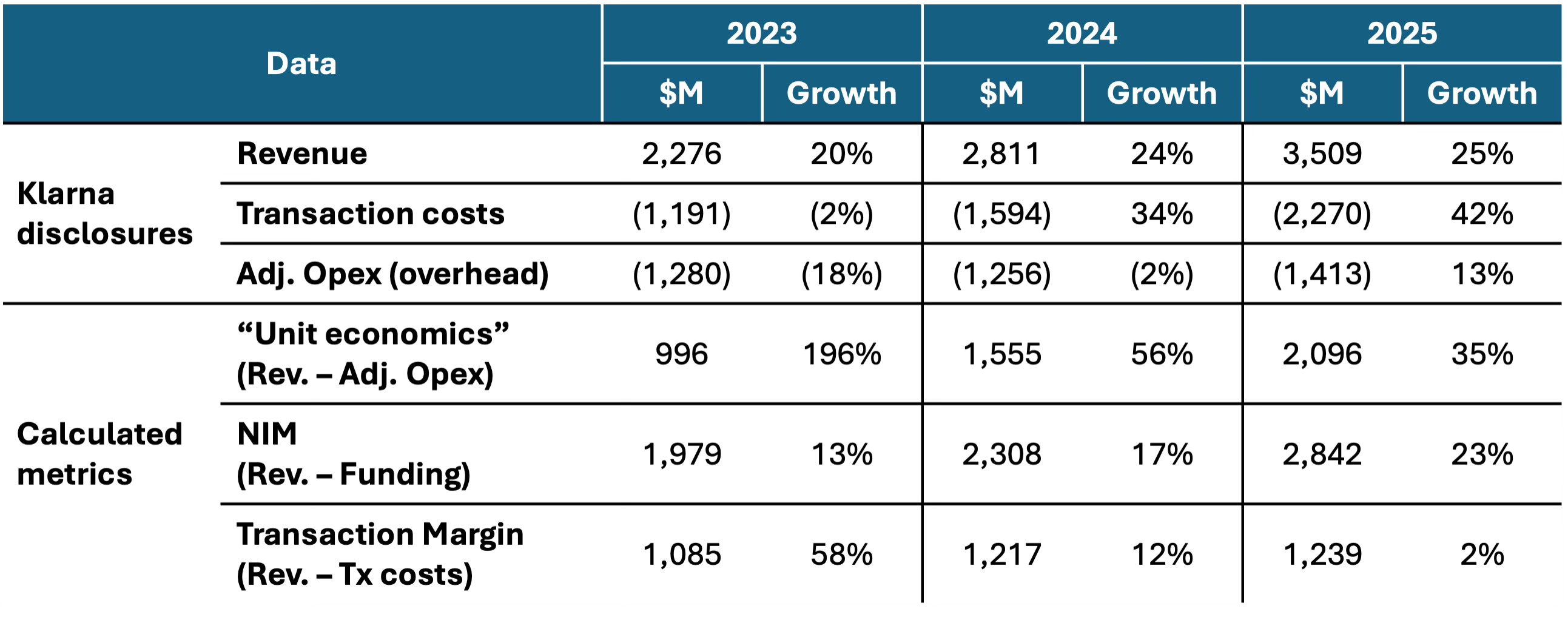

Klarna shows the following chart as evidence for its improving unit economics:

This chart has two key missing pieces that most Card Issuers would treat as contra-revenue items: Funding costs & Provision for loan losses. As it is, this behaves as if the gap between the Green line and the Purple line represent Contribution. They don’t. Here are the components from historical financials:

You can see why they want to focus on pure Revenue rather than Transaction Margin (TM, Revenue less variable costs). TM is barely growing as variable costs outgrow revenue (Funding Costs, Provision, Processing & Servicing Costs). It isn’t just Provision, which Klarna rightly points out is front-loaded. Processing Costs outgrew Revenue by 11% and Funding Costs outgrew Revenue by 8%.

Klarna’s Chart focuses cost on the relatively flat Adjusted Opex, i.e., overheads. Klarna’s presentation says: “Operating Leverage Continues as Revenue Outpaces Costs”. But Transaction Margin is moving in the wrong direction, which suggests they are not capturing economies of scale at the unit level.

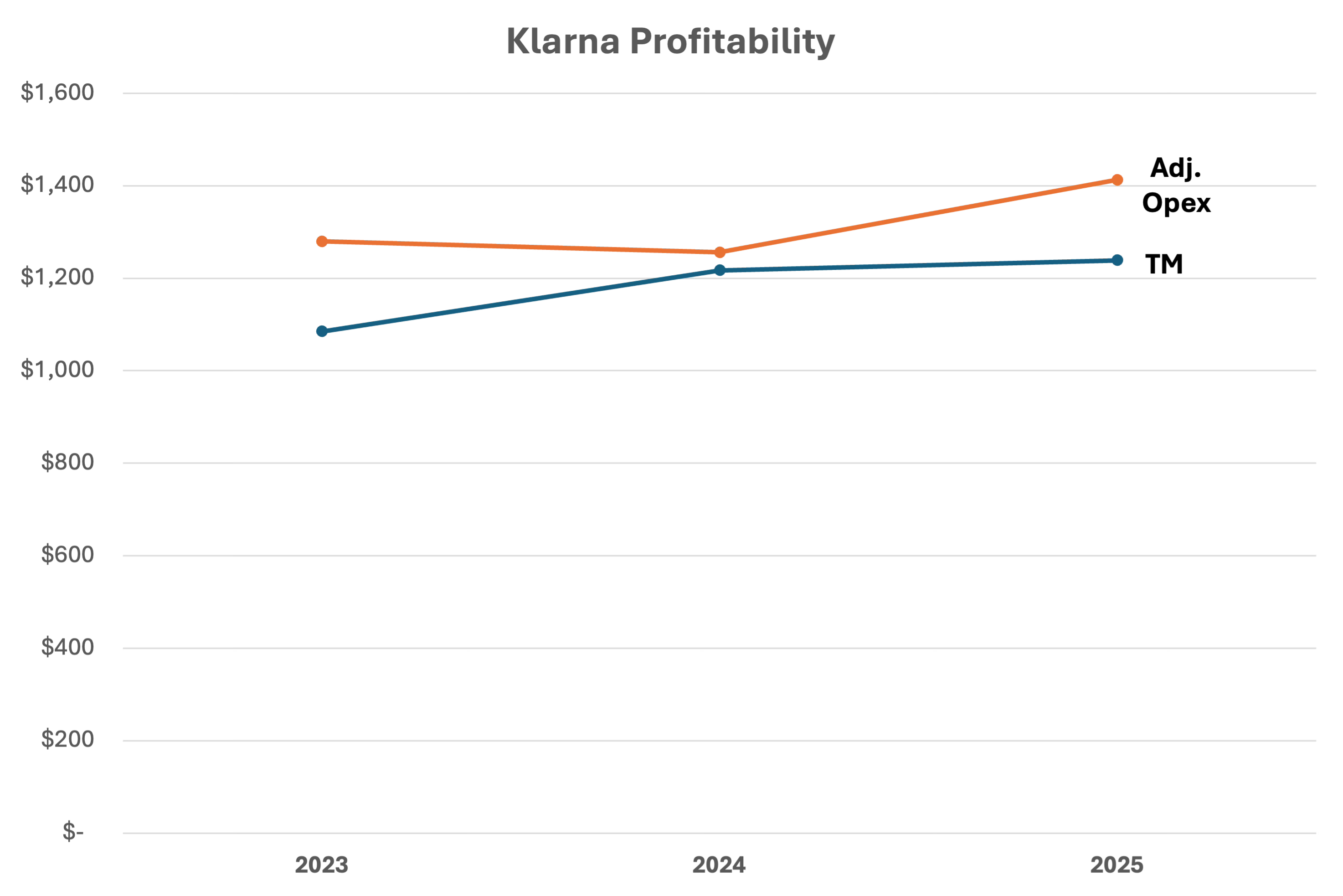

Focusing on Transaction Margin rather than Revenue shows that unit economics are improving very slowly. Here is the same chart that opened this section but comparing TM and Adjusted Opex instead of Revenue & Adjusted Opex:

The gap between the two lines effectively translates to Net Income which is indeed negative.

Provision as a % of TPV rather than a percent of loaned amount

Klarna shows a rosy picture of credit costs as follows:

They attribute the rise in recent quarters to rapid Fair Financing growth where the provisions are up-front but much of the revenue is post quarter-end. True; all long-term lending suffers this outcome with rapid growth.

What I take issue with is the continued use of GMV as the denominator (Gross Merchandise Value otherwise known at TPV). This may have been justifiable when most lending was Pay-in-4 but it just doesn’t work for Fair Financing.

Not all TPV is lent out, raising the denominator. Once the 37% of non-lending TPV is removed, the metric would be 60% higher

Q3 reported that ~20% of TPV is Pay-in-Full, so at a minimum the denominator should be reduced by 20%

25% of Pay-in-Four is paid up-front, so the loaned amount is 75% of purchase amount. That would reduce TPV by another 17%

TPV is as front-loaded as Provision. All TPV is the result of a purchase, so the complaints about up-front provisions distorting unit economics should offset this distortion

Fair Financing is a longer-term loan with likely higher credit losses. But it is mixed in here with the short-term, Pay-in-4 volumes that should have lower credit losses

I divided their 2025 provision by their reported 2025 consumer receivables and came up with 7.6% — a number that has been trending down. The equivalent calculation at Capital One yields 4.6%, although that numerator includes commercial loan provision, not just consumer – so the consumer metric is lower.

Funding costs and sources

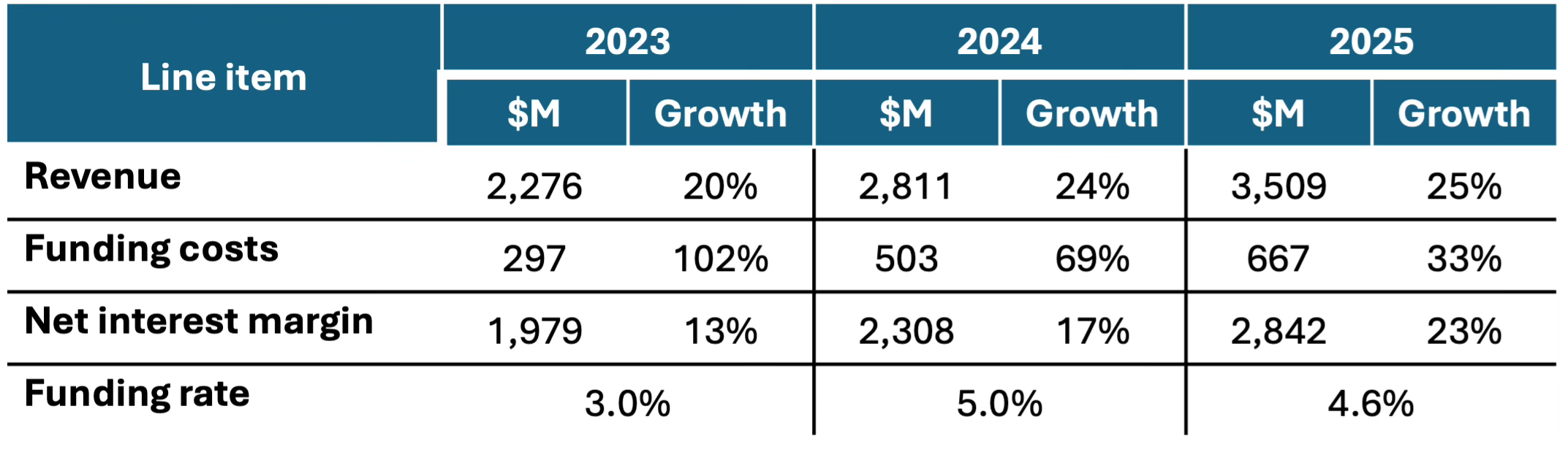

I noted in a prior section that Funding Costs were rising faster than Revenue. Here is the data to support that:

Through this period, Klarna’s funding costs have outgrown revenue, although the gap is narrowing: NIM growth has almost caught up with Revenue growth. Consumer deposits account for the bulk of funding over this period. The cost of those deposits rose with the rise in interest rates in the earlier years followed by the receding rates we are seeing now.

Klarna also securitized a portion of the Fair Financing portfolio, shifting the funding burden to a third-party. It also extinguishes the portion of provision on Klarna’s books, eliminating that source of noise. Most major consumer lenders securitize to a degree, but this is the first time for Klarna. They booked a one-time gain of $73M in that transaction. Securitization makes organic funding go further.

Can Klarna’s US banking strategy push those funding costs down? Their US “Balance” account does not get FDIC insurance. They pay rewards for spending, but no interest. The cash back rewards are only usable for more purchases with the Klarna App. To get higher rewards, customers can pay a monthly subscription fee. I suspect uptake is low, not least because Klarna don’t report on it.

Klarna applied for a US bank charter, although that may not solve the funding problem. High-yield savings rates are currently 3.5-4.0% APY. That isn’t much below Klarna’s 2025 funding cost given generally declining rates since then. 1-year CD rates, suitable to match-fund Fair Financing are going for 4% APY. Given the marketing and servicing costs associated with these products, the net impact on TM would likely not be material. Klarna would need DDA accounts to materially reduce cost of funds.

The track record of online lenders raising DDA does not provide much hope. In general, online banks, include from giant incumbents like AXP and SYF don’t raise much DDA. The Fintechs lenders that have tried have limited success.

Most consumers still prefer an branch-based incumbent for DDA, with a few affinity-based exceptions like USAA and Navy Federal.

Most Fintechs with bank charters don’t raise much DDA. SoFi grew a small bank into a $47B asset institution in just a few years. Deposits are 99%+ interest-bearing with a 2025 cost of funds of 2.5%. Even Schwab Bank ($250B+ in assets) has 99%+ interest-bearing deposits despite starting from an affluent population.

Klarna’s Pay-in-4 users will look more like Chime or Cash App customers. While those lenders have accumulated millions of Direct Deposit customers, deposit levels are not high. Many of those millions keep a primary DDA at an incumbent bank.

Given Klarna’s lending volumes, if it did have a charter it might be at risk of losing Exempt status over time. The $10B threshold applies just to US assets, but if Klarna USA keeps growing, they will eventually exceed the cap. That would make it hard to compete with the Neobank leaders.

Klarna could raise high-APY deposits in the US, just like it does in Europe, but that won’t reduce funding costs that much. I assess a low likelihood that their Tiered deposit accounts with subscription fees will raise material deposits at a favorable cost of funds.

Conclusions

Only vestiges of Klarna’s anti-incumbent snarkiness were in this earning release. They clearly anticipated how the market would respond to the disappointing metrics.

However, those metrics are not as transparent as I would hope for a maturing Fintech:

They focus on revenue growth rather than “transaction margin” growth. They mislabel their metric as “Unit Economics” when it excludes variable costs. As we saw, Transaction Margin dollars are growing slowly and that growth has declined over the last few years.

They focus on the slow growth of overheads (Adjusted Opex) rather than faster growing transaction costs. Transaction costs (variable costs) outgrew revenue in recent years. So while they have positive operating leverage relative to overheads, they are only slowly improving true unit economics

They focus on credit costs relative to TPV rather than lending volumes. That makes comparisons to industry norms very hard. While credit performance is improving, it underperforms relative to industry norms, albeit for a lower-FICO customer base

One can untangle the real story from their disclosures, but it would be a lot easier if they published industry standard metrics using industry standard definitions.

They also expect US deposit raising will help with funding costs, when it likely won’t. All major online banks raise interest-bearing deposits at high APYs, but few generate material non-interesting bearing transaction deposits. Klarna is unlikely to break the pattern with its tiered account and associated subscription fees. Charter or no charter.

Super read Andy. Painful! Public companies shouldn't drop 25% on earnings. FF seems a bit of a fudge to me.