Is Agentic Commerce good for Visa?

They think so, I don't

Key Insights in this post

An article in Payments Dive excerpted an interview with Visa’s CFO on Agentic Commerce; Mr. Suh asserted that Agentic Commerce would accelerate Visa growth in four ways:

Create more transactions by splitting purchases to optimize for price

Digitize more payments, reducing cash & checks

Accelerate B2B transactions

Increase overall economic production, stimulating commerce in general

In my view, the first three are unlikely or exaggerate benefits to Visa; the fourth is likely but from Generative AI overall rather than Agentic Commerce directly

Transaction splitting: Intelligent splitting may work against Visa revenue growth if the biggest merchants with the lowest prices gain share

Those merchants get big incentives from Visa to offset Visa’s fees

Those merchants get VPP deals, lowering interchange to issuers

Those merchants are the likeliest to adopt agent-assisted A2A steering

Digitization: Agents don’t accelerate digitization because cash & checks are not material in eCommerce

Agents may accelerate eCommerce at the expense of POS commerce, but eCommerce is much more concentrated that POS commerce, leading to those high incentive payments

Agents may steer customers to A2A where it can benefit a merchant and a consumer

Bill pay already shows signs of steering against cards with economic incentives and Open Banking. Agentic methods may accelerate this

B2B: Agentic Commerce doesn’t increase economic activity it simply redirects it to a different channel

Consumer spending does not increase just because agents help shop

Without more consumer spending, there won’t be more B2B spending

Economic Production: Production will rise due to GenAI’s productivity benefits; but Agentic Commerce does not increase consumer spending

Conclusions

No one can really predict these impacts, so Visa are smart to prepare for a major impact

However, if liability and data challenges persist, Agentic Commerce may retreat to “Agent-assisted search”, where it has limited impact on Visa

Visa’s own vision may result in lower Visa revenue, not higher

It channels more volume through the biggest, low-price merchants where Visa makes the lowest margins

The AIs themselves may qualify for network incentives; given the concentration in that market, those incentives would be high

Agents may steer to A2A to reduce merchant acceptance costs and generate their own revenue; that would reduce Visa volume

To make up for these impacts, Visa may need to impose Agentic Commerce fees, which makes A2A steering that much more likely

Introduction

I found an interesting article on Agentic Commerce in Payments Dive. Among other points of interest, it contains this observation:

“Payments players across the industry acknowledge that agentic commerce isn’t likely to arrive this year, and maybe not even next year, but they’re laying the groundwork now for what they hope will be a new form of digital buying and payments in the future.”

This aligns with my thinking.

The section I will focus this post on recounts an interview between my friend Tien-Tsin Huang of JPM and Chris Suh,Visa CFO:

We think it accelerates our opportunity to grow, and it does it in probably four meaningful ways,” Suh explained. These were the four points Suh made:

Agents “will just create more transactions – we think they’ll intelligently split transactions, and for us, transactions are a very important unit of measure in our business.”

Agentic commerce will further push payments generally in the direction of digitization, with fewer transactions happening in cash or check.

The commerce will accelerate business-to-business transactions.

Overall economic production will increase, spawning more commerce.

“When you add that all up, that’s just a bigger pool of opportunity for Visa to go after,” he said.

My immediate reaction was that the first three of these are either not likely, or they exaggerate the benefits to Visa. The fourth point would be true of any productivity improving initiative, especially Generative AI. In my view the productivity benefits of Generative AI will dwarf any specific benefits of Agentic Commerce.

Despite these bearish views, I think Visa should invest here. If Agentic Commerce becomes a mass market phenomenon, Visa needs to shape the ecosystem to be card-friendly. They have already established protocols that embed Visa Tokens as a key feature. Only if merchants use Visa tokens on Visa cards can they avoid liability. Smart move!

Even so, Agentic Commerce likely won’t lead to Visa revenue increases in the way Mr. Suh outlines. It is just as likely to do the opposite. Given my naturally skeptical disposition, you knew I would say that. But, I will show my work so you can decide for yourselves.

My general view on Agentic Commerce

I will briefly summarize my prior observations on Agentic Commerce as context for my comments on the Visa points.

Agentic Commerce requires autonomous payment

Without the payment, what many call Agentic Commerce is simply Agent-Assisted Search. Without the autonomous payment nothing at all changes for Visa. This outcome looked likely due to the liability issue. Assuming the merchant community accepts the Visa protocol to shift liability, autonomous payment is now technically possible, but whether consumers will use it remains an open question.

It should go without saying that Agentic Commerce won’t be useful for in-person shopping. Once a consumer is in a physical store, the agent can’t pay autonomously.

Agentic Commerce will be limited to a narrow range of categories

Agentic Commerce (AC) may be limited to standardized branded goods, where the Agent largely compares on price:

AC faces challenges with goods that rely on Taste & Fit, which are hard to model at the individual consumer level. Apparel, furniture, fresh food & housewares all rely on Taste & Fit and may be out of scope

AC faces challenges where the consumer doesn’t know enough about the category to write a specific prompt. I recently faced this with Snowblowers and Fire Pits. I couldn’t specify what I wanted until I had done my own research. These were high-ticket items with lots of options I didn’t even know I had.

In these cases, the consumer may need “Conversational Commerce”, where the agent educates the consumer on their choices to narrow down the decision. At the end of that process agent & consumer have jointly defined the prompt. But without that Socratic dialogue, the consumer doesn’t know enough to trust purchase to an agent. Once it has a prompt, the agent might seek out the lowest price, but if that purchase is only available at a limited number of stores, even that might be of limited value.

Agentic Commerce is fragmenting into walled gardens

Almost all the big eCommerce merchants block AI data scraping. They don’t want third-party agents taking their product and pricing data only to make a final decision purely on price. Instead, these mega-merchants are building proprietary AC services available only on-site. Among these merchants are Amazon and Walmart.

They will offer Agent-assisted shopping within their walled gardens, but in most cases, payment will be via Card-on-File, just as it is today (e.g., One-click on Amazon). In other words, within the biggest shopping venues, payment is autonomous, but not Agent-initiated.

Furthermore, by starving the third-party agents of data, these low-price leaders make those agents suboptimal for price optimization. If you ask an agent to get you the lowest price on a standard good, Amazon, Walmart, et al will not be among its choices. Yet those are the merchants that will often have the lowest price, particularly if shipping cost and speed are included in the cost calculation.

Agentic Commerce may steer against cards

Merchants hate Credit Card acceptance costs. They have sued the networks and issuers often on this topic. Steering consumers to lower-cost, A2A methods with lower acceptance costs hasn’t worked. The key barriers are rewards and grace period.

Consumer-side agents can easily calculate the value of rewards and grace period for any purchase and negotiate with a merchant agent to trade these away for a lower price. For example, If the acceptance cost is 2.50% on a $100 purchase, the merchant pays $2.50. The rewards to the consumer might be 1.5% ($1.50) and the 30-day grace period at 4% (current top APY on HYS) is worth 33¢.

That leaves 67¢ for the issuer and network: 16¢ revenue for the network and 51¢ net interchange for the issuer. The agent can split that between the merchant, the consumer, and itself with everyone better off financially except the card system stakeholders.

The Agent can get agreement upfront from the consumer to do this only if it is in the consumer’s financial interest – so any steering occurs before the transaction even starts, avoiding any network anti-steering rules. No consumer would bother with this on their own, but for agents, the math and negotiations take a nano-second.

Unlikely? Maybe, but the math is pretty simple and the outcome could be material on bigger ticket purchases or across all purchases cumulatively. After all, the consumer’s return is always higher than what their rewards would be and we all think rewards are the key blocker to A2A. The merchant comes out ahead every time.

Summary assessment

Agentic Commerce is coming, but may be limited to standardized, everyday goods where price is the only real decision. Since the biggest, low-price merchants may not participate, delivering the lowest price may be a hard promise to keep.

Agents may also encourage steering away from cards by negotiating with merchants in the consumer’s financial interest. Where the math works, the Agent can substitute A2A.

That sums to a bearish view on Agentic Commerce in general and for the networks in particular.

Visa’s four points

The Payments Dive article acknowledged that Agentic Commerce at scale is a couple of years out; no one has a more specific forecast on when it will happen, how it will happen, and what form it will take. My view was bearish, but the bulls could be right.

The rest of this post will assess each of Mr. Suh’s four points:

Agents will intelligently split transactions in the consumer’s interest

Splitting helps Visa because of it’s fee structure. Visa charges 14bps + 2¢ per transaction. If an Agent splits a $100 purchase bundle into four individual purchases, Visa gets the same 14bps (14¢), but it gets an extra 6¢ from the 3 new transactions. Note that it gets the same 6¢ lift on a $1,000 transaction although the bps are now $1.40.

But is that how it would work in practice? I don’t think so because it doesn’t account for shipping costs, network incentives, and interchange reductions.

Many eCommerce merchants charge for shipping if tickets don’t exceed a minimum. In my experience that minimum is usually ~$50. Even Amazon has a $35 minimum for not Prime members. It would be rare that the price savings are sufficient to overcome the shipping cost hurdle.

The more logical outcome is the most expensive item is carved out if it is >$50 and the other three remain bundled on a site like Amazon that has no minimum for Prime members and generally low prices (if not the lowest). In this scenario, Visa doesn’t get 6¢ extra but 2¢ extra. It’s total revenue goes from 16¢ to 18¢.

Network incentives

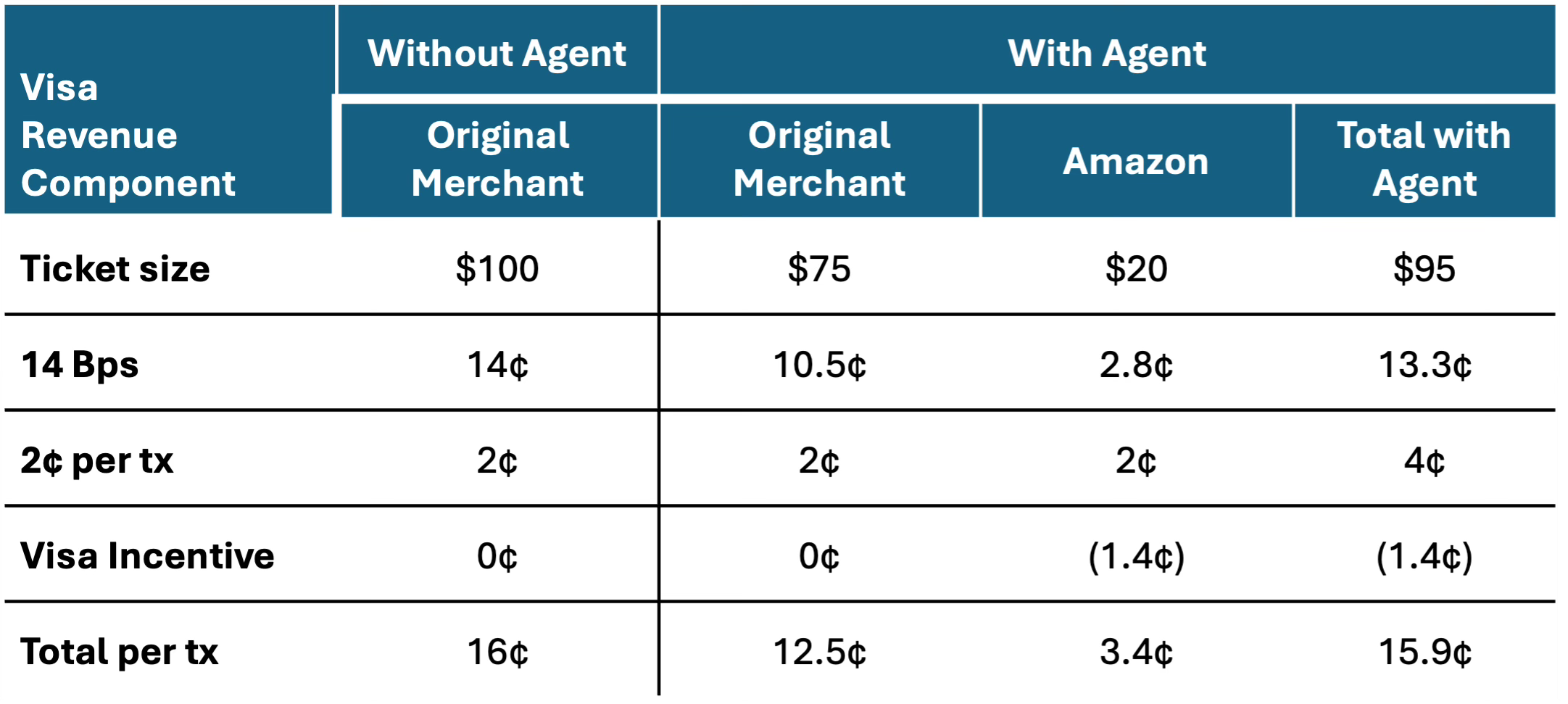

Of course, unbundling may not increase Visa NET revenue. Visa pays volume-based incentives to larger merchants. The highest incentives go to merchants like Amazon & Walmart who are the likely winners in a low-price competition (including shipping costs).

Consider a case where a consumer buys a specialty electronics good from a mid-sized merchant. That make and model aren’t available on Amazon and the merchant gets no incentives from Visa. The consumer bundles third-party accessories and a surge protecter in the purchase – commodity add-ons at high-margins.

The Agent optimizes for price and sends the add-ons to Amazon where the customer has Prime free shipping. Instead of paying $25 for the add-ons at the original merchant, Amazon charges $20. But Amazon also has incentives from Visa worth ~7bps per transaction (a total guess). Here is a table showing the economics for Visa in both scenarios:

Visa ends up with slightly lower revenue. It gets twice the revenue from the fixed fee, as Mr Suh predicted, but loses a bit on bps from the lower total spend, and it loses a lot from the Incentives to Amazon. If those Amazon incentives are lower, Visa might eke out an advantage.

The more volume that gets routed to mega-merchants the less lift Visa gets. If the bundle mix flips so that $75 goes to Amazon for $70, and $25 goes to the Original Merchant, Visa revenue drops by almost half. Transaction splitting may hurt Visa more than it helps.

Lower interchange

Splitting likely hurts card issuers. A handful of large merchants get VPP deals with reduced interchange. Amazon and Walmart are two of those VPP merchants. If Agents route volume to these low-price, VPP merchants, the issuers may lose half their interchange on those transactions versus non-VPP merchants.

That makes the whole ecosystem worse off in a price-optimizing Agentic world. The bigger the transaction, the worse off all the card stakeholders are. The only way that doesn’t happen is if smaller merchants offer the best prices. But that doesn’t make economic sense given economies of purchasing scale.

The more traffic going to VPP merchants, the less interchange there is to support generous rewards. At some point they will have to come down. But rewards are one of the moats against A2A steering. So even though Visa doesn’t share in interchange, its checkout position depends on high rewards.

Agents push payments to digitization

The argument here is that Agents leave even less reason to use cash and check.

The first problem with this argument is that eCommerce has virtually no cash & checks already. POS still has cash and checks but Agentic Commerce doesn’t work there. Both paper methods are losing commerce share even before Agentic.

Checks are declining at 7-10% annually and are rarely used in consumer commerce. Small Businesses use checks for supplier payments, not ad hoc purchases

Cash is still used at the POS, but average tickets are low (~$22) and usage is dropping. Even if Agentic Commerce worked in POS, savings on a $22 transaction would not be material in many cases and the consumer would have to travel to another store to capture them

The argument could be made that because of Agentic price optimization, Card-based eCommerce pushes out some POS Commerce and its associated cash and check use. That substitution has gone on for 20 years without Agentic.

It also ignores the steering challenge. As noted above, Agents might steer to A2A by optimizing acceptance costs for merchants & consumers at the expense of issuers & networks. Even without Agentic methods, small merchants on ISV platforms are using surcharges and cash discounts to accomplish the same thing.

Visa’s assertion assumes the merchants stay passive rather than arming themselves with agents. They can deploy new tools like surcharging that will become more accepted assuming the merchant settlement ever gets approved. I have written about the Adyen A2A steering capability based on advanced analytics. More of this will emerge as merchants or their vendors deploy agentic countermeasures.

The other check-centric use case is bill pay, where cards have made major inroads over time, but ACH is still king. Billers are already pushing back on card acceptance costs. All three major telcos now offer rich incentives to use ACH rather than cards. This is facilitated by Open Banking which makes it easy to onboard DDA account credentials. The Merchant Settlement may offer new tools. I expect this to spread to other Biller verticals that don’t already block or surcharge cards (e.g., loan repayments, tax payments, etc.)

Agentic Commerce will accelerate B2B commerce

I don’t understand this one. Do they mean that more consumer activity will ultimately result in more B2B activity? If so, the argument depends on an increase in consumer spend driven by Agentic Commerce. I don’t buy that.

Agentic Commerce doesn’t directly increase American’s discretionary income. It may stretch that discretionary income further due to price optimization, but it doesn’t directly increase incomes. Without higher income, the consumer won’t spend more. Without more consumer spend there is no follow-on increase in B2B spend.

I made the argument above that Agentic Commerce has virtually no economic impact on Visa. If consumers make the same card purchase in a new channel that doesn’t increase card spend. Almost all eCommerce processes on cards already. Where is the lift? Visa has more to lose here as some of that Agentic spend might get steered to A2A.

In terms of B2B on its own, cards are less of a factor. They dominate B2B2C use cases like Corporate Cards and they have some share of purchasing. The use of virtual cards in Account Payable, has grown fast. However, agentic methods are even more likely to steer B2B volumes to ACH or Instant than in retail.

Importantly, the average tickets are higher, so the buyer and supplier have more absolute dollars to bargain with than in lower-ticket retail. Further, the bulk of B2B already transacts on low-cost ACH that is easily transmutable to Instant.

One of the key value propositions of Virtual Cards is faster payment for accepting the card. Buyers could offer the same proposition via ACH, SD-ACH or Instant. It saves the supplier the card acceptance cost leading to higher likely conversion. By cutting out the issuers and networks, buyers & suppliers have more to split among themselves. Agents can negotiate these terms instantly.

Overall economic production will increase

They taught me in college that economic growth is a function of improved productivity, and Generative AI will clearly deliver that. The public data for Software Engineering productivity improvements show astronomical results, and that was previously an economic chokepoint. It will no doubt spread to other use cases and deliver equally compelling results. We are really just at the starting line.

But Agentic Commerce? I may be blinkered on this, but how exactly does it increase productivity? It could create more private time for consumers who do less research on major purchases, and it could make their discretionary income go further by seeking out low prices.

Unless that time savings get deployed to additional paid work it doesn’t increase economic growth. It is the same spend through a different channel

The consumers may save any benefit from reduced prices rather than spend it, which means economic production stays the same. Of course, this is not something Americans are famous for, but it could happen.

I am not an economist, so I am probably missing something here. Generative AI is a disruptive technology that should stimulate economic growth, but Agentic Commerce using Gen AI tools, doesn’t change much.

Conclusions

I have a more bearish view on Agentic Commerce than Visa. Being Visa, they may be right, but it isn’t a foregone conclusion. No one really knows. As I said up-front, networks and acquirers need to prepare for an Agentic Commerce future even if it ends up being anemic – like AC’s Internet of Things predecessor.

I also see boosters redefining Agentic Commerce downwards to mean “Agent-assisted search” rather than including autonomous payment in the definition. If that is the future, it has zero impact on the card ecosystem. The Agents tee up a purchase in a merchant’s checkout page, but the consumer still clicks the “purchase” button. They likely use the same card or wallet they would have used without the agent and Visa gets the same revenue it always got.

Even without an Agentic tailwind, low-price merchants like Amazon & Walmart are outgrowing eCommerce in general. Consumers may just use on-site Agent-assistants to make better on-site choices. In that case, nothing changes for Visa. Visa may get more volume from Chase’s Amazon Prime Rewards card and the Citi’s Costco Anywhere card but those economics are not attractive.

The worst outcome is the one that Mr. Suh outlined. Agents steer to the lowest price merchants, possibly splitting transactions along the way. That would concentrate spend on the least profitable venues for networks, issuers and acquirers. These mega-merchants are the most likely to implement A2A steering given their scale and their focus on low everyday prices.

Transaction splitting would suck the most profitable items out of the second-tier merchants, even if they hold onto their core offerings. Merchants often make higher margins on add-ons than on the core offering (e.g., Barbie clothes versus Barbie dolls). In short, it steers spend away from Visa highest revenue customers.

Even if Agentic Commerce takes off, I disagree with the statement: “When you add that all up, that’s just a bigger pool of opportunity for Visa to go after”. I don’t think so: It is the same quantity of commerce switched through a different channel. And it may be a smaller revenue pool for Visa as commerce shifts from smaller, high net-revenue merchants to big, low net-revenue merchants.

A final point is that none of this reckons with the AI companies’ revenue needs. They may be willing to execute AC for free, but more likely, they want to be paid. That can come from consumers, merchants or card system stakeholders. If it is the later, it could be the networks paying incentives just like they pay big merchants or acquirers; given AI concentration, those incentives could be huge.

The way out of that future is for Visa to impose incremental merchant fees for Agentic Transactions. That has two predictable outcomes:

It raises the ROI from A2A steering, making it more likely

It engenders outrage among merchants, who may launch new lawsuits

On the other hand, my favorite saying is “Never bet against Visa”. If their revenue is at-risk, they will impose the fees and put up with the outrage.

Thanks for the comment!

I can think of ways to deal with the Taste & Fit issues but they take a lot of upfront work by the consumer to train the AI. For example, you could take pictures of all your favorite clothes to train the Agent before you send them off to shop. They could then present you with their top finds and you pick the one you want. The Agent then buys it. Given most of these purchases are intermittent, it probably isn't worth it.

In terms of the "customer knowledge" issue, I think the conversational commerce model would help even without closing the loop to the purchase. The purchase is actually the easy part!

In terms of your parasitism point. Agentic Commerce is a modest step beyond Google Shopping: The consumer enters the product they want, and Google already shows them the best options & pricing. AC goes a step beyond that to pick from the options and compete the transaction.

This is one of the most thoughtful and well analysed pieces on agentic commerce I've seen to date. I do wonder if it's worth pondering over what it would take to avoid the bearish outcome where all we get is "agent assisted search". How does one solve the challenges related to autonomous payments to make them a reality?

Also, building on your points around "taste & fit", and "lack of customer knowledge", what is the consumer behaviour unlock we need for autonomous payments to truly become a thing? Any new payment method historically (e.g., credit cards, debit cards, BNPL, UPI, PayPal, contactless cards, Apple Pay, etc.), has won by solving a pain that was previously unsolvable, and by latching onto a habit people already had. New payment behaviour is rarely created; it is borrowed from an existing daily act. It's parasitism of sorts. What might that be for autonomous payments?