Incumbent Acquirers face 3 disruptions

Incumbents are keeping volume but ceding revenue

Key insights in this post

True disruption is rare in Financial Services and usually triggered by regulatory action

Acquiring was disrupted in the 1980s and faces three disruptions today

In the 1980s, Electronic Draft Capture (EDC) displaced paper vouchers leading banks to exit and nonbanks to dominate, particularly FDC

More recently acquiring faces three disruptions, by ISVs (e.g., Square), by global “gateways” (e.g., Adyen) and by eCommerce platforms (e.g. Stripe)

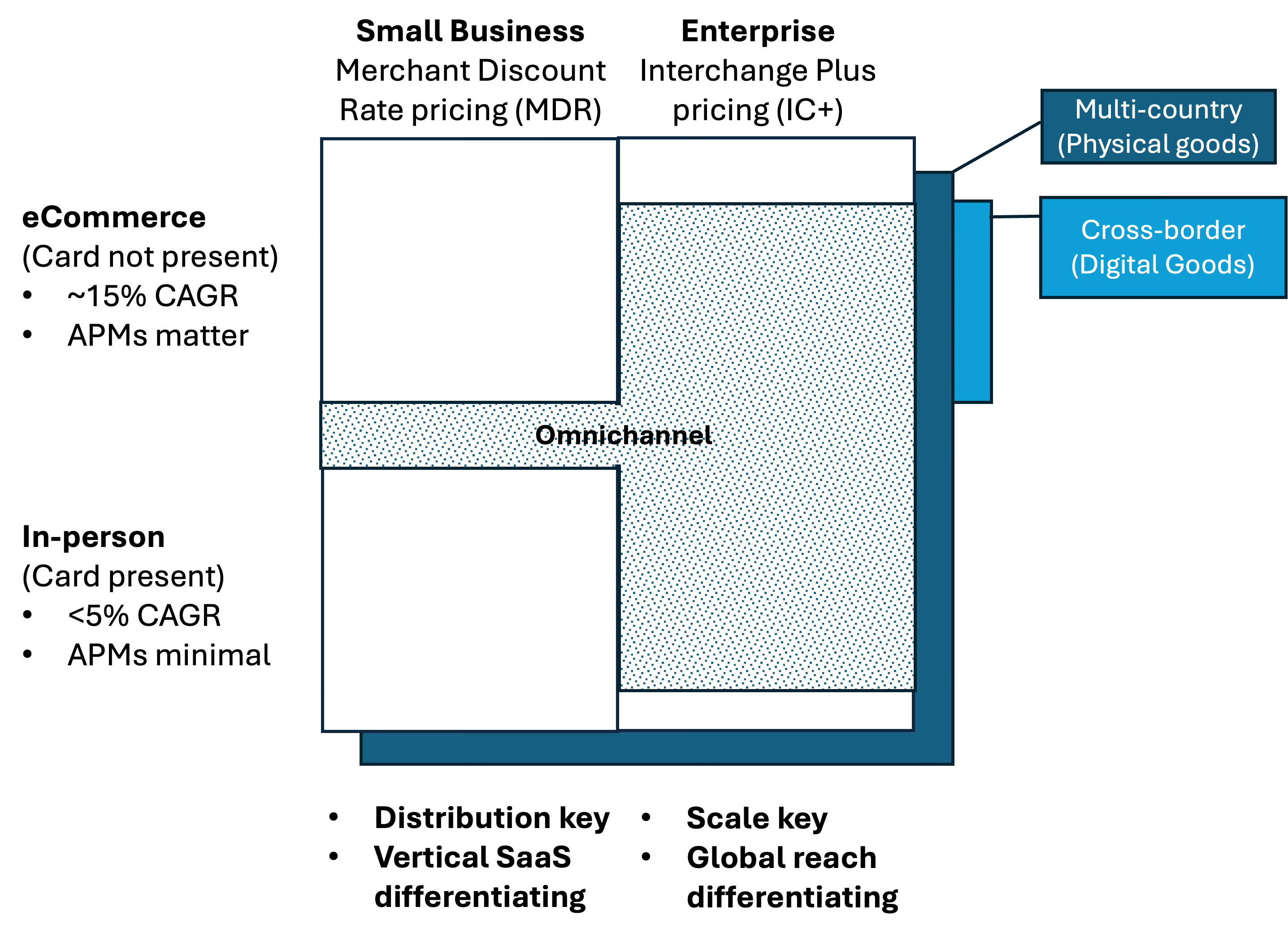

We can visualize what is happening in a three-dimensional framework:

Columns: Small Business & Enterprise, which differ by revenue model

Rows: eCommerce and In-person which differ by growth rate. The distinction is eroding with the emergence of Omnichannel, particularly in Enterprise

Depth: Domestic vs. Multi-country vs. Cross-border which differ by complexity

Insurgents have emerged in three of the four domestic quadrants

Small Business, in-person. ISVs have displace POS-terminal-based incumbents. Exemplified by Square

Small Business, eCommerce. Platforms have displaced pure acquiring. Exemplified by Stripe alone and by Stripe in combination with Shopify

Enterprise eCommerce. Global gateways can deliver 100+ countries and hundreds of Alternative Payment Methods (APMs). Exemplified by Adyen

The remaining bastion of incumbents is Domestic, In-person, Enterprise

Incumbent scale makes them competitive even at very low transaction fees

They process for most insurgents, keeping the volume but giving up revenue

Even in their bastion, insurgents are nibbling at the edges

Incumbents are targeting quadrants dominated by the insurgents with varying success

Acquiring was particularly vulnerable to disruption:

It is less regulated than other sectors, so regulations were not an entry barrier

The shift to eCommerce changed the risk profile and skills required

The linkage of acceptance with business software changed the terms of competition

WARNING: This is a particularly long post. Find a comfy chair and have a warm drink handy to get through it!

Introduction

I have always found merchant acquiring fascinating because it has been disrupted not once in my career but 4 times. This is not just change, but disruption in the Clayton Christensen sense: an insurgent targets an underserved segment and then expands.

The first disruption happened around the time I joined financial services. Paper vouchers were still the most common capture method and most banks still had acquiring units. Banks specialized in voucher capture due to proximity and similar skills in check processing. Over time, the industry shifted to EDC (Electronic Draft Capture) on POS terminals. EDC shifted the advantage to nationally focused, scale processors, especially First Data (then owned by American Express).

Eventually most banks sold their acquiring businesses to nonbank acquirers or formed Joint Ventures with them. As a result, First Data alone processed over half of US card transactions. The banks became distribution channels for FDC and other nonbank processors. Price pressure led to 80%+ concentration in the top 10 processors – and concentration continues to this day.

As recently as the early 2000s, we all suspected the end game was in sight – and in a sense, we were right: Today, the top 4 incumbents process 80%+ of domestic volume (Fiserv/FDC, JPM, WorldPay, & BAC).

But revenue share has fragmented away from these incumbents. The high-margin small business segment attracted insurgents who capture the retail margin but outsource processing at a wholesale price. Different insurgents served POS merchants and eCommerce merchants.

The fast growth, digital goods merchants required global acquirers who could support local payment methods beyond cards. Insurgents got a premium for the local methods, the obscure geography, and the value of a single integrated solution.

A different iconic name led the way in each of the fast growth segments:

In-person, Small Business: Square. Square pioneered the “Integrated Software Vendor” (ISV) model where payment acceptance is bundled with vertical business software. Newer ISVs then fragmented the segment by vertical

eCommerce, Small Business: Stripe. Stripe + Shopify pioneered the digital version of an ISV; Stripe provided the payments while Shopify provided the digital store. Stripe also directly powers most digital start-ups off Shopify (e.g. ride share, Airbnb)

eCommerce, Enterprise, Cross-border: Adyen. Adyen pioneered the global gateway model that helped digital goods companies sell in any country and accept any payment method. Previously, global merchants needed separate acquirers in each country

In my mind, these represent three distinct disruptions that happened simultaneously. Today, all the insurgents are moving towards the incumbents’ remaining bastion: In-person enterprise. There are also invading each others’ quadrants. Incumbents are not standing still – they too are adding vertical software, geography, and payment methods to stay competitive.

This post will flesh out this framework. It will show how insurgents took advantage of technology and market change to tailor solutions to narrow segments. As they all enter each other segments, a battle royale is emerging towards a new end-game.

Acquiring framework

The diagram below maps the modern acquiring market:

The columns represent the revenue model for small businesses versus Enterprise:

Small Businesses are charged a Merchant Discount Rate (MDR) – a percentage of transaction value. The acquirer themselves pays the Interchange and Network fees from its MDR proceeds. This model reimburses the acquirer for the bankruptcy risk of small merchants since the acquirer must make good on any trailing chargebacks

Enterprise businesses are charged on the Interchange+ model (IC+) – interchange and network fees are passed through at cost while the merchant pays the acquirer a flat fee per transaction; this can be as little as a fraction of a penny per transaction for very large merchants

Both models can be high margin: MDR if the acquirer has efficient distribution and IC+ if the acquirer has processing scale. The difference is in aggregate margin not percentage margin. In MDR, volume is low but price per transaction is high, in IC+, price per transaction is low but volume is high.

The rows represent the commerce venue:

In-person merchants, Card Present (CP). Card data are captured by a POS device

eCommerce, Card Not Present (CNP) Card data is either typed in (guest checkout), on file, or transmitted using a digital wallet like Apple Pay

Omnichannel merchants who operate in both CP & CNP:

In Small Business:

Most brick & mortar merchants are primarily CP

Many digital pure-play merchants are starting to open physical stores, but the bulk of volume is still CNP

In Enterprise, almost all merchants are Omnichannel.

Verticals like QSR now have material order-ahead and delivery volume – which is CNP even if fulfilled in a physical store.

Pure-play digital merchants are becoming rarer as many open retail stores, but digital goods merchants still have no physical presence

Depth represents geographic reach. Acquirers globalize to follow their biggest customers:

Top panel: US domestic. The US has few Alternative Payment Methods (APMs), mainly PayPal. Other countries have more APMs and those APMs account for a greater share of volume. Most in-person merchants are US-only

Middle panel: Multi-country acquiring. Merchants selling physical goods in a limited set of countries. Few physical goods merchants operate beyond 20-30 countries. ISVs become multi-country to access more TAM, not because their clients go global.

Last panel: Cross-border, digital goods merchants. Digital Goods merchants have no physical fulfillment so can operate in any country if they can accept payments there. These verticals include streaming media, online gaming, & social networks. They need APMs to satisfy consumer preference in each country. Acquirers focused on digital goods often reach 100+ countries and hundreds of APMs. Note that the Cross-border panel only serves the CNP row and the IC+ column – to be truly global, a merchant needs to be big

The next section will review each quadrant of the domestic panel. I will refer to the global panels as relevant.

Quadrant Champions

In each quadrant I focus on a single, iconic company that represents the business model. Typically they were one of the earliest entrants.

eCommerce, Small Business (Upper left)

This quadrant is exemplified by Stripe & Shopify. Although they operate independently as well, their strength is partially a result of their symbiotic relationship. Pre-pandemic, PayPal had a leadership positions in this space, but the explosion of DTC (Direct to Consumer) start-ups in the pandemic overwhelmingly chose Stripe, Shopify or the combination.

What this delivered was a turnkey solution that allowed a small merchant to have big-merchant capabilities fast.

Stripe could be integrated with just 7 lines of code. Their solution was built on a cloud native, API-centric infrastructure that allowed quick integration and frequent innovation. Stripe also sped up ancillary processes like KYC and underwriting to get start-ups in business fast

Shopify gave small retailers a fully functional storefront in a drag-and-drop model. They focused on making the online merchant’s life easier, adding features like loans, consumer lending & fulfillment. Shopify powerd merchants representing as much as 15% of eCommerce

Each of these companies has competition, but competitors are smaller and don’t provide as comprehensive a service. Both companies are growing into adjacent quadrants and the global dimensions:

Working with Enterprise-class companies (Stripe now serves Amazon). Often this is because small customers have grown to become Enterprise class

Becoming global (150+ countries), often to follow their customers as they globalize

Moving to the physical point of sale (Stripe Terminal, Shopify POS)

Adding value added services like loans and payroll

In-person, Small Business (lower left)

Square pioneered the ISV story I told two weeks ago. Pre-Square, this quadrant was a one-size fits all market where all small businesses got a generic POS terminal and an opaque, “qual/non-qual” price schedule. What differentiated acquirers was distribution.

Bank-based acquirers distributed through their branches. As banks sold off their acquiring arms they remained a distribution channel for their partners – usually First Data (now Fiserv). ISOs had independent sales forces that proactively called on small merchants. Other channels included Associations, VARs, and even Retailers. But everyone was selling the same POS Terminal + Merchant account service.

Square entered the market at the very low end. The original gimmick was a dongle that turned a smart phone or tablet into a POS Terminal. This appealed to micro-merchants who didn’t want to spend hundreds of dollars on a conventional POS terminal and often had limited volume. It also made card acceptance mobile. But, the dongle was only one of five innovations Square pioneered, and not the most important:

Software. Square loaded their service with free, basic software that helped a small merchant manage their business. One delivered Inventory Management. My first encounter with a Square merchant was at a school fair; the merchant sold T-shirts and their 7-year old son checked me out. He visually looked up my purchase on his tablet and tapped the screen when he found it. That transferred the sale price to checkout and then he swiped my card through the dongle. This seems trivial now but was revolutionary then. Square eventually built software for four verticals: Retail, Restaurants, “Appointments” (e.g., salons), and Invoice-based businesses (e.g., caterers) – thus beginning both the ISV model and the verticalization trend

Pricing. Square pioneered all-in-one pricing with a single MDR for all card types. Prior to this, the merchant faced “qual/non-qual” pricing: a rate for Qualified transactions (generic credit cards) and a series of Non-qualified rates for more obscure card transactions (e.g., commercial cards, affluent cards, small business cards, etc.). It was hard to tell what the all-in MDR was until you got your statement and did some math. Further, the acquirer passed through increases in interchange and network assessments 2x per year – and took the opportunity to increase their margin each time. I had a merchant friend with a Qual rate of around 2% but an effective rate of 4.5% because his acquirer had pushed through so many price increases on his non-qual rates. When he switched to a new acquirer, his effective rate dropped to 2.5%. Merchants vastly preferred the transparency of all-in pricing

Underwriting. In the incumbent model, acquirers manually underwrote the merchant’s credit risk as if they were lending them money. This could take two weeks or more. Square turned on merchants almost immediately and managed the credit risk via limits. The merchant started with a low limit, which was raised as they demonstrated good behavior. This was much faster than the old method although it did incur more losses. It allowed Square to onboard micro-merchants that other acquirers wouldn’t touch

Hardware. Because each merchant was using an off-the-shelf mobile or tablet as the logic engine, the dongle could be simple & cheap ($5). When Square started serving more established merchants they sold a plastic frame to hold a tablet that looked more professional. Merchants often repurposed used tablets or phones to keep the cost down. This simplified hardware fulfillment compared to incumbents who had to ship POS terminals. It also allowed cloud-based software upgrades where POS Terminals had to be updated in-person

Distribution. Square used a self-service model to source and onboard customers. The dongle was available on J-hooks at office supply stores, and even at Starbucks, in addition to online. To get the advantages of #1-4 above, lots of small merchants were willing to sign-up online and use on-line self-service. Square didn’t need a field sales force until it started moving up-market. It didn’t need bank branches and its didn’t have to partner with ISOs

Today’s ISVs routinely use most of these innovations. The Dongle was replaced with a Bluetooth “hockey puck” which itself is being replaced with tapping directly on a phone or tablet; but most ISV platforms use an OEM tablet to serve up their software. That Software is increasingly vertical as exemplified by Toast. While ISVs employ a sales staff, they have much higher rates of inbound sales than incumbents. And almost all of them use flat rate pricing. Only the underwriting model has not caught on, although that may be because conventional underwriting has become more efficient.

As a result, a great sucking sound can be heard from most conventional acquirers. High margin small merchants sign up with ISVs, and the ISVs process through a scale incumbent. But the ISV captures the margin and pays as little as a penny per transaction to the processor. The incumbents kept the volume but lose most of the revenue.

Most of the big incumbents have adopted the ISV model with mixed results. Fiserv has success with Clover. JPM & BAC only recently licensed software from NCR. USB/Elavon acquired Talech. Worldpay missed the trend and Global Payments tried an M&A route where the jury is still out.

The challenge is that each vertical needs dedicated software, which is expensive to develop and scale. In general, Vertical-specific ISVs are winning versus cross-vertical solutions. Exhibit A is Toast, a restaurant specialist, who may have as much as 50% share of the attractive targets within its vertical (as discussed two posts ago).

Major incumbents and insurgents are pursuing similar growth strategies:

Offering CP merchants CNP services to become Omnichannel (e.g., order ahead)

Migrating towards Enterprise by serving small chains

Adding new verticals (Toast just began serving food-related retailers)

Becoming multi-country (Toast just entered Canada)

Adding services on top of payments, particularly lending, AP, & payroll

eCommerce Enterprise (Upper right)

I struggle defining this quadrant as “disruption” in the Christensen sense, because most of the merchants served are large & global. Unlike Stripe & Square’s original focus on small business, Adyen went after globe straddling digital goods merchants right from the start. Those merchants were indeed underserved by incumbents, but they weren’t small by most measures.

eCommerce launched a new kind of merchant: digital goods. These included streaming media, online gaming & (legal) gambling, eBooks, VPNs, social networks, and crypto. These businesses did not have physical fulfillment needs, so could rapidly globalize. They were only limited by their ability to accept payments locally. In many countries that was not just cards but all kinds of alternative payments methods (APMs) like wallets, pay-by-bank, installment loans (e.g., Klarna) and local debit schemes.

The card networks made it unattractive to accept cross-border card payments through their interregional surcharges; so merchants contracted with a local acquirer in each market and directly connected to APMs. That entailed a lot of work. The original “gateways” connected to a portfolio of local acquirers and APMs so the merchant could integrate once to accept all methods in all geographies. The gateways abstracted away all the complexity.

From the start, Adyen was a leader in this space. They had the broadest geography and the widest array of APMs. All of it was built on a technologically modern platform. They got their own banking license to be a direct participant in the Networks, reducing potential points of failure. Only the original Worldpay (then part of RBS) had similar breadth – and they only had it because they bought the original startup founded by Adyen’s founders!

The beauty of all this was that cross-border digital goods was the fastest growing vertical in payments. It routinely exceeded 40% annual growth. So even if you didn’t bring on any clients, you got a 40%+ tailwind from your clients’ organic growth. Of course, Adyen did bring on lots of new clients as well.

Eventually they diversified into omnichannel support, originally for luxury goods merchants. These merchants had big online sales couple with a thin global store network. They were small in each country, and treated that way by a local acquirer, but they were big as a global business. Adyen developed POS capabilities to support stores and treated the merchants as unified clients, reflecting their global volume. They have repeated this trick in other verticals.

Adyen also pioneered higher authorization rates for eCommerce by working directly with issuers. That gave Adyen eCommerce clients higher conversion rates on the same volume. Other acquirers eventually copied that trick, but Adyen is consistently on the leading edge.

When Adyen started, digital goods was a tiny vertical that was ignored by incumbents. But it grew into a meaningful base from which Adyen built scale. The were born global but have expanded into the other quadrants in their own unique way:

They serve omnichannel, enterprise-class merchants in the lower right – usually from a global entry point

They serve “Platforms” that themselves serve the two small business quadrants

Adyen gets the volume without the distribution costs

Adyen provides embedded banking products like lending & deposits for their platform partners to white label

In-person Enterprise (Lower right)

In the US, this quadrant supports four scale providers (FI, JPM, Worldpay, BAC) and a couple of vertical specialists. These four companies process for virtually all the largest brick-and-mortar retailers. This quadrant has the most volume but the lowest prices per transaction. For a scale processor, it is high margin, but they need lots of volume to cover overheads.

JPM may process more volume, but Fiserv is the more interesting story. Fiserv bought First Data (FDC) in 2019. FDC was built on a cascade of acquisitions and Joint Ventures that gave them 50%+ share at the point when KKR took them private (2006). They have since lost their JVs with JPM and BAC and are restructuring their JV with Wells.

At one point, three of today’s scale acquirers plus Wells & PNC were all processed under the FDC umbrella. Since then, this quadrant hasn’t been so much disrupted as fragmented. The loss of JPM & BAC were triggered by change of control provisions when FDC went private (JPM) and acquired by Fiserv (BAC). The Wells JV simply expired.

One of the trends causing that is the emergence of ISVs. The old model used Enterprise volume for scale and SB volume for profits. As ISVs emerged, most incumbents were happy to process their volumes at wholesale pricing. In the early days, those prices had generous margins; but, as ISVs grew, pricing dropped. FDC still provides this kind of processing under the “Clover Connect” brand.

Clover is Fiserv’s captive ISV. It was originally a hardware acquisition, but FDC converted it to the ISV model. Clover is distributed through bank branches, VARs, ISOs, and inbound. Restaurant is the biggest vertical, mostly in counter service, like Square. They have Retailer clients, but are not as vertically tailored for retail sub-verticals as many ISVs. It is a similar situation for other business types like Appointments.

In other words, their solution is more horizontal and appeals more to smaller merchants who don’t need advanced functionality. It is a half-step above the legacy terminal model, but not verticalized enough for many use cases. In fact, many Clover clients just use the Clover Flex device as a POS Terminal – without meaningful software use. Fiserv offers the full array of add-on services like Clover Capital loans, payouts, etc.

Carat is their product for CNP Enterprise. From my understanding it is primarily a multi-country solution to help physical retailers be Omnichannel rather than serving cross-border digital goods companies. That also means cards are more important to the proposition than other APMs. So, while Adyen starts in CNP and helps clients become Omnichannel in CP, Fiserv starts in CP and helps clients become Omnichannel in CNP.

Still, Fiserv/FDC is actively counter-attacking the disrupters:

They are the leading player in Enterprise CP and added omnichannel functionality to cement their position. They have a scale moat as any insurgent will absorb a lower price per transaction compared to their home quadrant

They use Clover to compete in the lower left quadrant against Toast, Square, etc.

They use Carat for global Omnichannel

They seem focused on multi-country, CP merchants who become omnichannel

They seem less prevalent in digital goods where Adyen is the market leader

They don’t have a branded solution for the upper-left quadrant where Stripe leads

Why was acquiring so vulnerable to disruption?

A few financial services products have been as disrupted as Acquiring:

The displacement of Pensions with 401Ks

The displacement of deposits by money market funds in the Reg Q era

The emergence of Neobanks as a result of stimulus payments, relying on Durbin

In these examples one kind of financial institution takes share from another kind – usually via regulatory arbitrage. Pure, competitive disruption is rare, likely because financial services regulations create barriers to entry. But acquiring is relatively unregulated, so regulations are not a moat.

In some cases, the insurgents took share, but plateaued. Think of the Apple Card now that Goldman won’t be subsidizing it or the displacement of revolving credit by installment credit through Fintechs like Affirm and Klarna. Or the robo-brokers. These initially looked like mortal threats that ultimately reached a ceiling.

I have shown that Acquiring is an exception. The EDC era displaced banks with nonbanks and more recently the likes of Stripe, Square, Adyen have taken real share and revenue from entrenched, scale incumbents. Why?

If we go back to Christensen’s Innovators Dilemma, it wasn’t just that insurgents entered a market serving an underserved segment, it was that the insurgents competed on a different dimension than the incumbents. For example, Compaq computer competed on portability rather than price/performance. Luggable computers had worse screens, slower speeds, weighed a ton, and were more expensive; but for consultants like me, they were a godsend. Over time they got lighter, faster, and cheaper, to evolve into today’s laptops – which now have equivalent price performance for most use cases.

I think something similar has happened here. All the iconic insurgents exploited market inflection points to expose an underserved market. Those inflection points were the emergence of eCommerce and the emergence of new technologies:

eCommerce

When eCommerce emerged around 2000, it accounted for a small share of retail sales and had much higher fraud, chargebacks, and returns. From an acquirer’s perspective it was high-risk coupled with low volume. When FDC and JPM split before 2010, JPM got most of the eCommerce volume (Paymentech) while FDC kept most of the conventional merchants. That seemed rational at the time, but Paymentech got Amazon and several other large eCommerce merchants. When I joined JPM in 2014, Paymentech claimed to process half of US eCommerce.

Paymentech focused on domestic, Enterprise eCommerce. They did move to Europe, but 5 US-based clients accounted for 90%+ of volume at the time. During my tenure they didn’t expand outside the EU & North America, they didn’t integrate with APMs, and never reached down to serve smaller eCommerce businesses.

That left room for Adyen (cross-border digital goods, APMs) and Stripe (small business, eCommerce) to emerge. Both Adyen & Stripe had competition from other Fintechs, but the entrenched incumbents didn’t keep pace.

Cloud software & Mobile technology

In Small Business, In-Person, JPM helped incubate Square in return for getting to process all their volume. But Square grew so quickly that it qualified for the lowest wholesale rates quickly. Lot’s of incumbents tried to roll-out dongles to compete, not understanding that all 5 innovations were needed (Software, flat-rate pricing, self-service, fast underwriting, and hardware). It is only in the last couple of years that JPM & BAC rolled out their own ISV solutions while WorldPay still hasn’t.

Square took advantage of the widespread availability of cheap, advanced mobiles and tablets. Instead of distributing expensive, dedicated POS terminals, they repurposed the smart devices the customer already had.

Square also developed business software to take advantage of the processing power and big screens of those devices. Using cloud technology, they could update the software constantly to add functionality or fix bugs. Stripe & Adyen obviously deploy cloud software for the same reasons, but that is more natural in eCommerce.

Conclusion

The overall conclusion is that acquiring insurgencies happen when incumbents miss the potential of emerging technology because it was initially useful only in high-risk, edge use cases. By the time insurgents blaze a trail, it is hard to catch up.

It is also clear that incumbents tried to fit new technology into their legacy business models while insurgents built the business model around the technology. Incumbents built dongle solutions, but they sold them as auxiliaries to conventional terminals – for example, to provide mobility for an outdoor dining area.

Recall that FDC bought Clover for its elegant hardware, and only later evolved it into an ISV solution. The original plan was to build a software marketplace on Clover so other developers could support business functionality. Eventually FDC/Fiserv had to go into the software business directly.

This pattern will sound familiar to readers of the Innovators Dilemma, but it has been enlightening to see it play out in real time.

The evolution of the acquiring business is one of the best case studies of gradual but material change in the structure of financial services. The disregard that many banks had for merchant services led to many bad strategy decisions (exit, partnerships, JVs, consortiums) but also to a lack of flexibility when the value of being at the commercial nexus became apparent (loyalty, rewards, BNPL, etc). As always a great read Andy.