Handicapping payments Fintechs

Why I admire some Fintechs but not others

Key insights in this post

Not all Fintechs are payments Fintechs as I define them

I define a Fintech as under 20 years old using modern technology. That excludes incumbent financial processors operating on legacy technology

Not all Fintechs are payments Fintechs that actually processes payments. This post only addresses payments Fintechs

I outline the key factors I look for to predict payments Fintech success:

Operate a B2B or B2B2C distribution model to moderate customer acquisition costs

Target narrow verticals or use cases to differentiate from incumbent horizontal providers

Born global to generate FX income and differentiate from more domestically focused incumbents

Capture growth via “share of wallet” in addition to new customers

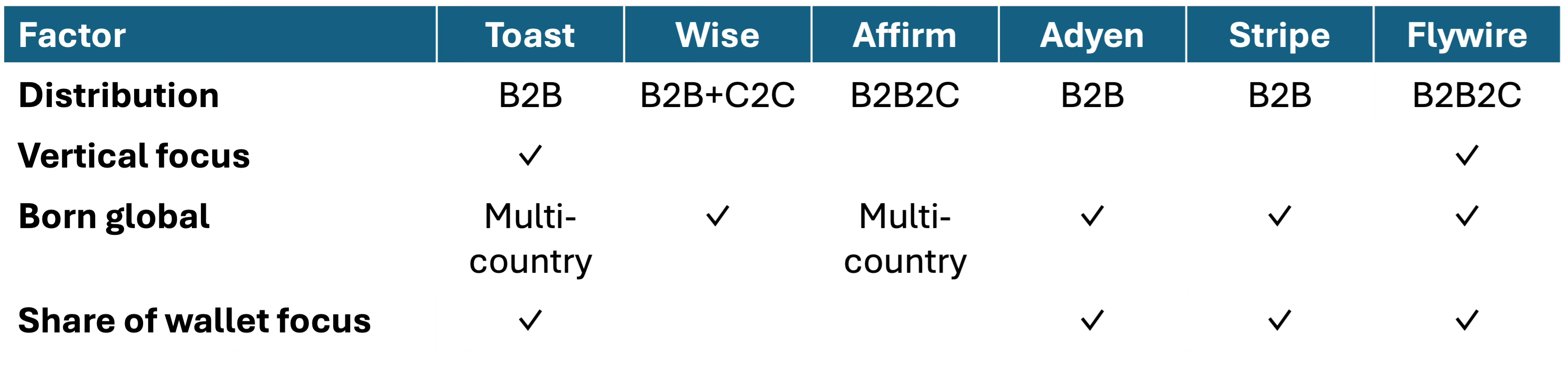

The six Payments Fintechs I profile each meet half or more of the key factors (Toast, Wise, Affirm, Adyen, Stripe, & Flywire)

Distribution model is the factor most commonly met

All have a global dimension or are globalizing

Only two are vertically focused, while most pursue share of wallet

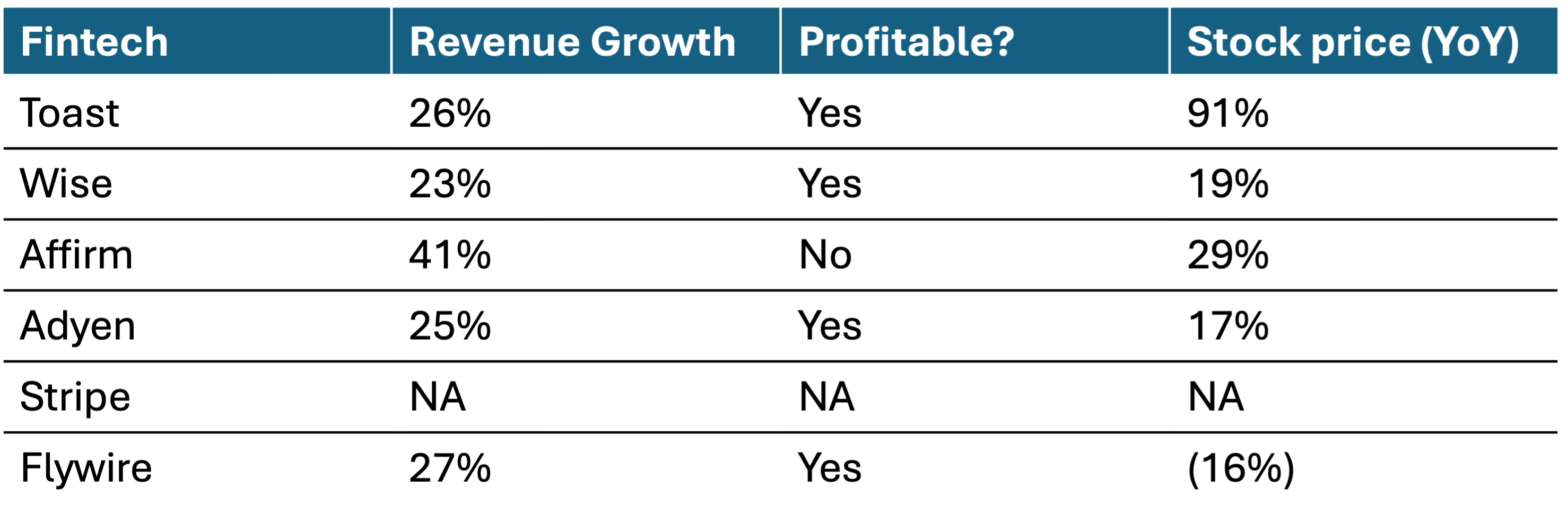

The group all show high revenue growth, but inconsistent stock price movement

All six show high revenue growth within a relatively narrow band

Despite similar revenue growth, Toast had the highest stock price growth while Flywire stock was the only one that declined

Affirm is the only one with a net loss, but had high stock price growth

Flywire is the laggard on stock price but met all the factors;

Nevertheless my view is that they are on the right track over a longer term

Note that this is a strategic assessment not a stock recommendation

Introduction

One could get the impression from my 25 published posts that I have a bias against Fintechs. That would be wrong. I am indeed skeptical of Fintech hype that begs to be deflated. But, I am actually a big fan of certain payments Fintechs including Toast, Wise, Affirm, Adyen, Stripe, and Flywire. I think I say complimentary things about them when they come up.

In this post I will lay out the key success factors I look for in payments Fintechs and how these payments Fintechs stack up against those factors. As a reminder, I own no individual equities, don’t manage my own investments and I am not an investment advisor. I did a short project for one of these companies when I was a consultant, but we lost money on it, so I don’t think it biases my assessment.

Some of these companies are not producing exceptional financial results yet, but I think they are on the right strategic path.

What qualifies as a Payments Fintech?

The first issue is: What is a Fintech? The term has been stretched beyond recognition. Many incumbent financial processors have rebranded themselves as “Fintechs” because they compete in the financial technology space. Technically, this is true, but it generally rubs me the wrong way.

I use the term to describe relatively young companies that process on modern technology – usually, cloud-native and API-centric. Some incumbents are moving to the cloud and re-architecting around APIs, but they are not fully there. Note that some of my favorites are almost 20 years old and Public – they are not scrappy startups anymore.

Second, the term “Fintech” includes non-payments companies serving wealth, lending, financial management, etc. I do not have informed opinions about those sectors. Others Fintechs provide SaaS platforms but don’t process payments themselves. So, my full definition is: youngish Fintechs using modern technology to process payments transactions themselves.

That definition leaves some companies on the bubble. For example,

Affirm is primarily a lender but it processes purchase transactions and competes with an incumbent payments product — credit cards.

Plaid moves information that can support payments, but Plaid does not itself execute those payments

For my idiosyncratic reasons, I think Affirm qualifies as a payments Fintech while Plaid does not. Plaid does provides risk management data for ACH (i.e., it checks the DDA balance before its client submits the ACH), and that is payments adjacent – but that is only a small part of its business today. So Affirm is in and Plaid is out. I still admire Plaid and if they ever do process payments I would add them to my list.

Key success factors

I have biases on what factors make a payments Fintech attractive:

Operate a B2B or B2B2C distribution model. Distribution is the key challenge in any Retail-focused business (consumers & small business). The B2B model serves companies while the B2B2C model uses an intermediary to aggregate consumers. Both of these are a more efficient ways to grow volume than direct to consumer (DTC).

As one example, Affirm does B2B2C by distributing through merchant web sites. This lowers to cost of customer acquisition and provides Affirm a pipeline of new customers which they can monetize in their marketplace.

Verticalized in fragmented verticals. It is rare to find a big horizontal market that some incumbent doesn’t cater to. Many Fintechs succeed by narrowly focusing on the needs of verticals or narrow use-cases. Toast is the poster child for the vertical approach — until recently they focused on single-location restaurants and small chains. They have even tailored the software for sub-verticals such as Bars, Hotels, catering, etc.

These specialized Fintechs embed themselves into the workflows of their customers, making them hard to displace. For example, Stripe’s APIs make them an integral part of a merchant’s business. Vertical-focused Fintechs do this to a greater degree than horizontal Fintechs. This does not exempt a Fintech from price pressure as clients get larger, but it slows those price declines compared to less integrated competitors.

Verticals or sub-verticals with a large middle market may be the most attractive as distribution costs are lower and margins are still healthy. Very large clients demand very low pricing, so they are not attractive early targets even if they bring a lot of volume. The smallest businesses are expensive from a distribution perspective.

Wise focuses on a use-case — FX — rather than a vertical. For use-case focused Fintechs, the equivalent to a fragmented vertical is a fragmented provider market. If there is no giant incumbent with high share, the Fintech can compete on some dimension that the incumbents are not as good at. Wise was early to the digital channel where the incumbents were still mostly focused on the in-person channel. Arguably Adyen & Stripe did the same thing in Acquiring, they focused on eCommerce where the incumbents were mostly focused on the in-person market. Adyen further focused on the cross-border, digital goods sub-vertical.Born global. Focusing on global needs confers advantages:

It is hard to do, creating a competitive moat; compliance is a particular challenge

It supplements transaction fee income with FX income

It may offer price premiums for obscure geographies and payment methods

The best example here is Adyen, which has served 150+ countries and several hundred payments methods almost since inception. They started by serving the Digital Goods vertical; these companies can serve the entire globe if they can just get payments acceptance in each country, including local payment methods. The long tail of countries and methods represent incremental revenue to digital clients, so they are willing to pay higher fees for access.

I distinguish between cross-border and multi-country strategies. Cross-border strategies serve truly global companies while multi-country strategies serve local needs in several countries. The most common way to globalize is to follow customers as they globalize, with Stripe as a recent example.

But any Fintech serving small business is likely multi-country, such as Toast. Affirm distributes through larger companies, but only operates in a handful of countries. Adyen, Stripe, Wise & Flywire are fully cross-border.

Share of wallet focus. Fintechs, by definition, operate on modern technology, which facilitates continuous improvement. However, the ability to innovate and the willingness to do so are separate things. During the boom, Financial Sponsors prioritized volume growth over profits so Fintechs could invest well ahead of revenue. Some of that investment was well targeted and some wasn’t.

The ones I admire invest strategically. It doesn’t always work, but the odds are higher. The ones I disdain chase “TAM expansion” without a clear path to success. Wise relentlessly invested in their core business while some competitors squandered resources on diversification before they had solidified their core.

Toast is a master at this. Their entry point is POS software plus payments, but they have added lending, payouts, AP, Payroll, reservations, kitchen management and other services on top of that entry point. Upsell & Cross-sell are always less expensive than sourcing new clients. Further, the more services each client consumes, the less likely they are to defect.

Share of wallet strategies don’t work well with Enterprise customers, because they look for best-of-breed in every use case. That makes it harder for enterprise-focused companies like Adyen to pursue share-of-wallet. They have diversified into payouts, accounts payable and similar adjacencies but I suspect these are not sold as a bundle but rather as individually priced add-ons. In its earlier years, the equivalent share-of-wallet strategy for Adyen was adding more countries and payment methods rather than adjacent functionality.

Do my Fintech criteria hold up against my Fintech list?

The table below shows how each of my admired Fintechs maps against my criteria:

Select Payments Fintechs assess against key success factors

I was surprised at these results. In particular, Flywire has the best fit. Here are the YoY financial results as of Q3 to see if the framework predicts performance:

The criteria seem to predict revenue growth but not stock price. Affirm is the outlier in a weird way – they have the highest revenue growth and the number two stock price increase, but they are the only one that lost money: $100M as of Q3. Go figure!

Revenue growth for the others cluster in a narrow range of 23-27% YoY, which is well above market growth. Stripe is NA because they are not public, but likely have high revenue growth.

The only common thread is that none of these 6 are exclusively direct-to-consumer (DTC) — which reflects my selection bias. Wise has the most DTC volume and the best stock performance, so this refutes the framework. Perhaps, Wise’s focus on a single, global, horizontal use case explains that outcome. Affirm and Toast are also focused but both only recently went global – they were not “born global”. Stripe, Adyen, and Wise are more horizontal than vertical.

Flywire had the best fit but the worst stock performance

If the criteria are valid in toto, Flywire should be the top performer since it is the only one that meets all criteria. They grew revenue faster than all but Affirm and became profitable in 2024, but were the only company that had a stock price decline. This is an object lesson that my readers should never invest based on my commentary! I rely on a third-party money manager, not just to avoid conflicts but because I am a terrible stock picker.

I don’t want to misquote my Equity Research friends, but when I talk to them about Flywire, they say that the story is confusing. Flywire serves four verticals, with dominant share in one. There is concern they may have topped out in that vertical —Education. They don’t get a lot of credit for the share-of-wallet initiatives, and there is a wait-and-see attitude on their newest vertical – Luxury Travel. There was also macro noise around a Canada regulation. In general, my analyst friends don’t see a clear story. The other names on the list have more straightforward business models.

I won’t argue against any of that, but I think the key difference is time horizon. Analysts have a more detailed grasp on the near-term financial indicators (up to 3 years?). But I take a longer-term view (5+ years?). At this point, someone should quote Keynes that “in the long run we are all dead.” I embrace that criticism.

So what makes Flywire so special? I think Flywire is building a scalable two-sided platform for cross-border B2B2C use cases. They have added four use cases to that platform, but could add new ones at low marginal investment. They integrate tightly with the “B” side of the transaction and are adding new features that solve more of those clients’ challenges. Effectively, they are creating a Global B2B2C network that could move money cross-border for any use case in almost any country.

Distribution Channel

The advantage of the B2B2C model is that the Fintech gets retail margins without retail marketing costs or the retail compliance risks. Consider the cross-border tuition use case: Flywire collects money from foreign student via local payment methods and moves those funds to a university in the destination country — usually in a developed country. The university promotes the service to their students for convenience and cost reasons:

The money is posted into the university’s ERP, reducing administrative costs

The student pays using a local payment method in a customized local portal

The FX rates are competitive

As compared to credit cards, it is lower cost due to network cross-border fees

This last point is important. The card networks impose cross-border fees on top of Interchange that can add over 1.5% to the total cost. Flywire focuses on high-ticket use cases (e.g. Tuition), so those fees add up. This is a form of network arbitrage, similar to what I described a few posts ago. Network cross-border fees amount to around one-third of network revenue, so are likely not going anywhere unless governments attack them. That creates a moat for Flywire’s services.

Flywire does not have to market its services to the same degree as other FX players because they are operating in a closed-loop: their business clients do the promotion because it is in their interest to do so.

Because the receiver is typically a university or hospital, AML risks are lower. That contrasts with Wise who moves money among individuals or small businesses where there is a greater KYC & AML burden. Flywire’s new vertical, Luxury Travel incurs more AML risk, but not as much as P2P.

Verticalized

Flywire serves Universities, Health Care, and Travel – with some B2B. It tailors services to each of these, and has a direct integration into client ERPs, but the consumer portals on the send end are standardized although white labelled for each client. In other words, no matter how many new verticals or business clients it boards, the sending end is already built and just has to be branded.

Flywire ERP integrations reduce the client’s administrative headaches, and makes the Flywire service difficult to displace. In some cases those ERPs are themselves vertical, such as EPIC for hospitals.

Born Global

Flywire only enters verticals that need a C2B FX service. It earns service fees on processing and FX margins on conversion. Compared to the domestic margins for C2B transactions, it has more revenue sources and higher transaction margins.

FX works like any other enterprise market, the more volume you process, the lower the fees from your providers. So as Flywire grows, it’s FX margins should improve.

Share of Wallet focus

Flywire has done a series of acquisitions to anchor itself in its verticals and to add new capabilities, but the most interesting organic innovation to me was their addition of “payment plans”. Flywire operates in high-ticket verticals where the consumer may find it difficult to fund the transaction in a single payment. Payment plans allow the receiving business help their customer stretch those payments over a longer period. Flywire provides the technology while the business provides the balance sheet – there is no credit risk involved.

This contrasts with Affirm which does a similar thing with lower ticket, commerce purchases. Adyen, Stripe and Toast also lend, but they do B2B lending via Merchant Cash Advances, at least partially on balance sheet. Flywire only administers the payment plans without financing them – avoiding the credit risk.

Conclusion

To summarize, most of my admired companies meet over half my criteria. The criteria seem to predict strong revenue growth, but not necessarily strong profitability or stock price increases.

Only Flywire meets all my criteria. Their revenue growth has been strong and they became profitable in 2024. This is remarkable given their core verticals went close to zero during the pandemic. They are building what amounts to a payments network devoted to cross-border, non-commerce, C2B use cases. Their pricing advantage is due to high Card Network cross-border fees that are unlikely to change. Their compliance advantage is that they work with receivers who are not obvious money laundering vectors. The network is scalable for new use cases, particularly on the consumer side.

So Flywire’s challenge is, can it add new cross-border verticals and volume to scale their fixed infrastructure? If they can, network economics take over.