Clarity could kill some stablecoin yield models

That incents Fintechs to get bank charters

Introduction

I have generally thought the rhetoric on stablecoin yields is overblown. After all, so-called Cash Management Accounts have been around for 40+ years and do pretty much the same thing.

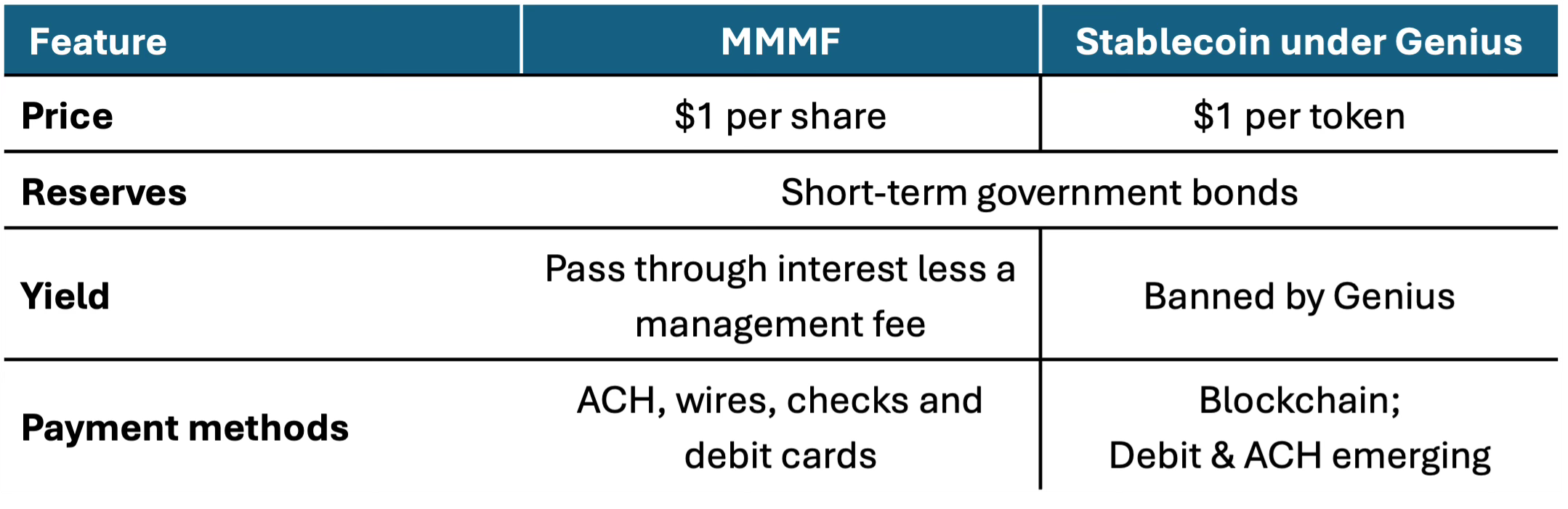

Stablecoin reserves regulation under the Genius Act are similar to those imposed on MMMFs. Stablecoins are effectively an MMMF attached to a blockchain. That makes payment easier if the counterparty accepts blockchain. Today, Stablecoins use debit cards or ACH for payments since almost no one other than crypto exchanges accept them as a medium of exchange.

The big difference is that Stablecoins under Genius cannot pay yield. The objection is that this would undermine bank deposits without bank regulatory obligations. I take no position on that debate as I don’t know enough about the regulations. As a principle however, I believe in level playing fields.

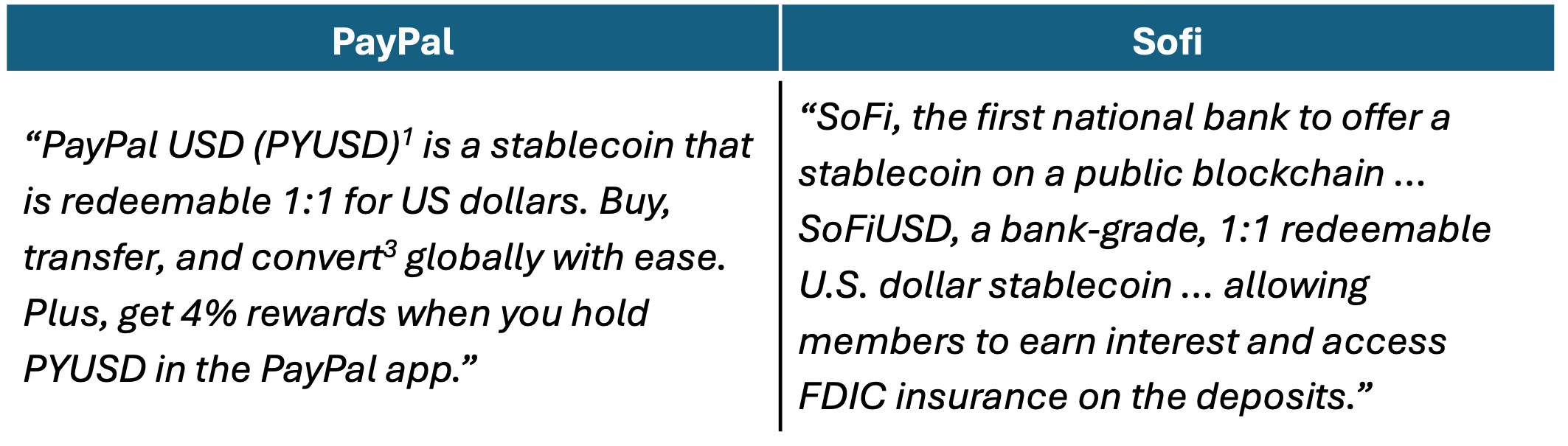

Which brings us to today’s topic. We saw announcements of a SoFi stablecoin this week, that pays yield. Furthermore, PayPal’s PYUSD still pays “rewards”. How can they do that?

When I looked into it, I found that fintechs are finding loopholes to Genius even before the final rules are published:

Two other fintechs announced stablecoin initiatives that don’t pay yield: Robinhood will receive yield from the Global Dollar Network stablecoin, USDG; but, it will not pass that yield through to customers – citing Genius. MoneyGram launched MGUSD, for its traditional cross-border use cases, but does not seem to pay yield to holders.

So how can PayPal & SoFi pay yield when MoneyGram & Robinhood cannot?