Chime shows progress

Revenue growth, but no profits … yet

Key Insights in this Post

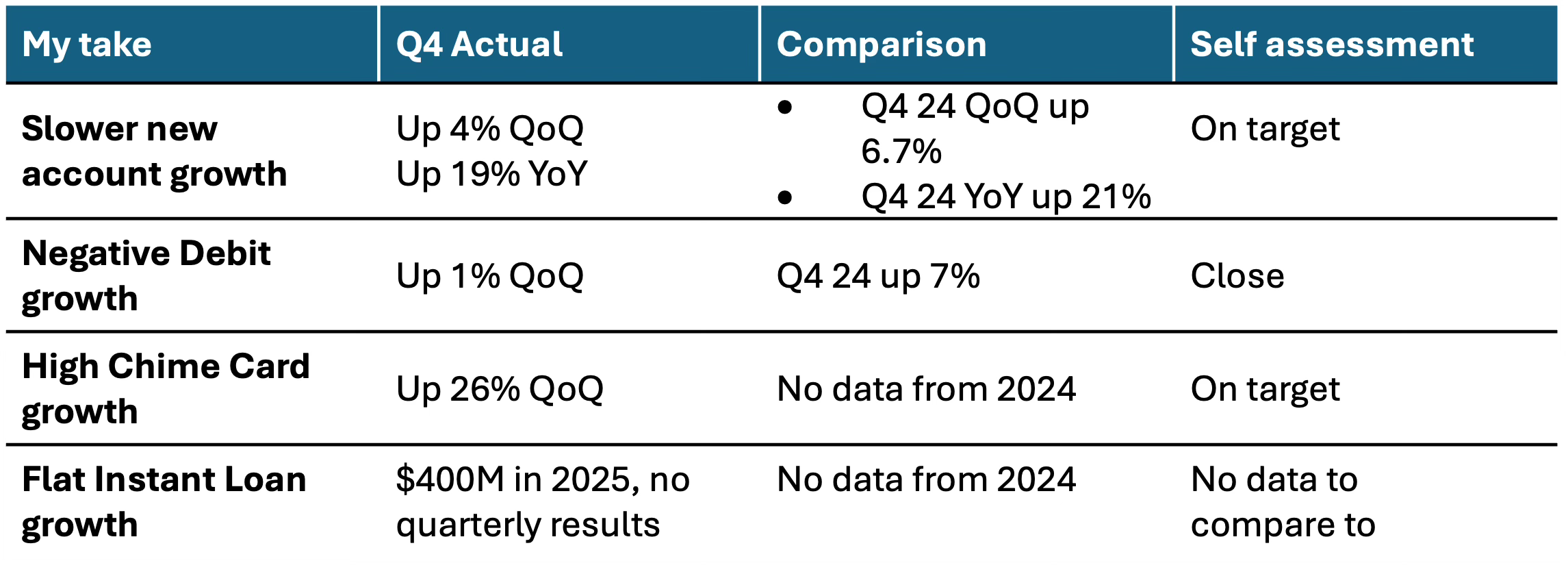

Chime’s Q4 earnings showed revenue growth that was directionally in line with my estimates a few week ago (based on BIN-sponsor data)

Eccentric metrics still that mask actual performance

Account growth benefits from a very forgiving definition of “Active” (1 transaction per month) and “Primary” ($200 in direct deposit OR 15 purchase transactions)

After implementing equivalent forgiving definitions Cash App became 50% bigger than Chime in Primaries and 6x in Actives

In neither case are all these accounts actually primary as most customers also maintain a bank account

Operating leverage metrics are distorted by using Revenue as the denominator. Using Transaction Profit in the denominator shows poor efficiency but better progress on operating leverage

Revenue growth is impressive

Payments revenue grew because Chime converted Debit users to Chime Card users.

As a secured credit card, Chime Card earns higher interchange

Rewards costs reduce the Chime Card advantage over Debit, even though Chime Card’s rewards proposition is very narrow

Chime Card faces a 50bp reduction in IC if the Merchant Settlement goes through. At the capped IC rate, rewards reduces revenue below debit

Lending revenue grew from MyPay and Instant Loans

Instant Loans are relatively new

They may have 15% penetration of Primaries, overlapping with MyPay

The high APR may limit addressable market

MyPay advances have reached maturity after <2 years in market

Penetration of Primaries may have reached 88% with ~2 advances per month, i.e., almost 1 per pay period

Credit losses hit the 1% target

Growth now depends on new Primaries rather than adoption in the base; the Enterprise bank-at-work initiative is a promising way to grow those primaries

Conclusions

I came away from the Q4 presentation with a more optimistic view

Chime should still refine metrics to give a clearer picture of performance

Strategically, they seem on a positive trajectory

The Chime Card genuinely increases revenue without increasing risk. The merchant settlement would undermine its value

Lending products have tapped into an insatiable demand for short-term credit in the Chime demographic, but may approach saturation quickly

The key for 2026 will be growing Primaries, not Actives. These provide the low-CAC base for all the high growth products. Disclose Primaries!

Introduction

A few weeks ago I published a post on Chime that examined the Call Reports of their BIN Sponsors to see what it told us about likely Chime performance. Now that Chime Q4 earnings are out we can check whether I had it directionally correct or not:

Not terrible given all the confounding factors. I should have said “Declining Debit growth” in my post, which is what I meant, and then I would have nailed Debit, getting 3 out of 4. Given my guidance was directional, this performance is not really impressive. But it wasn’t way off either.

This post will assess actual progress in the following broad areas:

Areas where the disclosures mask actual performance

Account growth

Efficiency Ratio

Areas that demonstrate real progress

Payments growth (TPV & Revenue)

Lending growth

Areas where disclosures mask actual performance

To repeat myself, the way Chime defines some metrics shows a sunnier picture than if more standard metrics were used. To be clear, any definition is arbitrary, and Chime’s metrics track their definitions, but the result exaggerates progress.

Account growth & ARPAM Growth

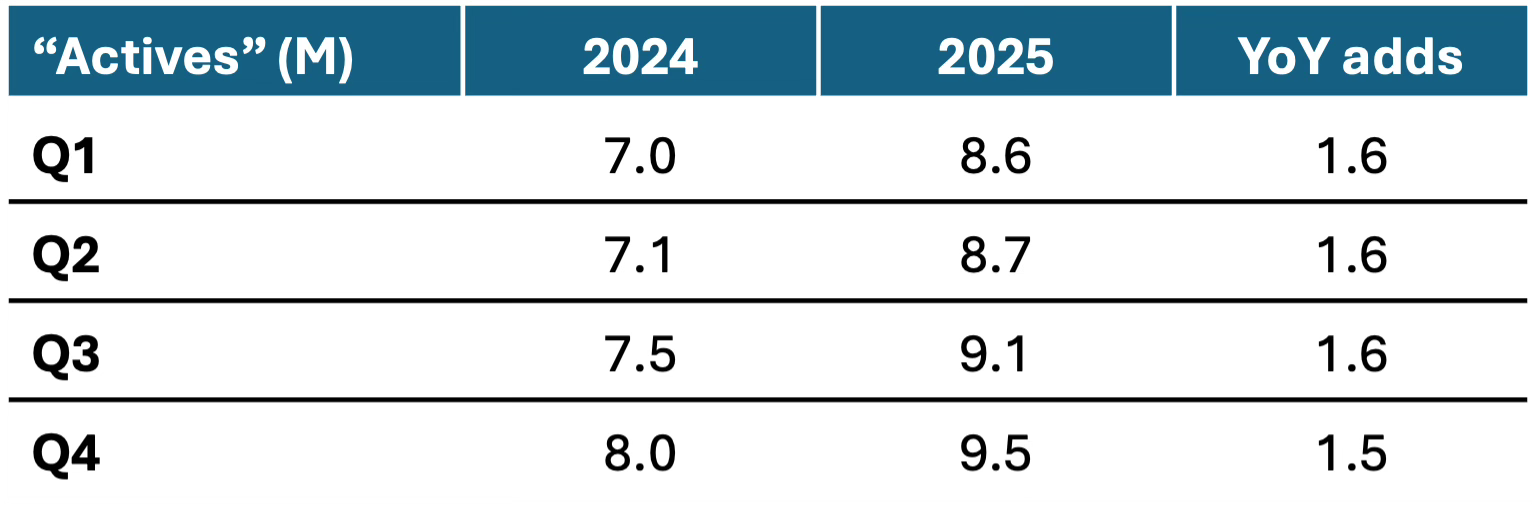

Something odd is going on here. Active Member growth followed the same pattern as 2024 and added almost identical numbers of Active Members.

Their definition of “Active Member” is forgiving:

“a member who has initiated a money movement transaction on our platform in the last calendar month of the applicable period”.

1 is not Active! They point out that Q1 has higher active members due to Tax Refund deposits. That implies those accounts were inactive in the prior period, i.e., no money movement at all.

Their definition of “Primary Active Member” is also forgiving: One direct deposit >$200 OR 15 purchases on a Chime-branded card:

$200 monthly inflow implies annual income of $2,400, unlikely for a true primary

15 purchases is just under half the activity of a typical debit-centric user

Many of the accounts Chime labels as Primary are likely secondary. Evidence for this is their focus on OIT revenue which charges a hefty fee to move money from a customer’s Chime account to their external bank account – likely the true primary.

This growth compares with Cash App growth of “Primary Banking Actives”. Cash App uses modestly more forgiving “Primary” criteria than Chime:

Receive inflows of any size (not including P2P). Given how low the $200 Chime limit is, I consider these equivalent

Spends at least $500 per month “including Cash App Card, Cash App Pay, Afterpay, or ACH bill pay”. $500 in debit spend would be 10-12 transactions. So, this standard is more forgiving than Chime’s

Like-for-like, Cash App may have 50% more “Primaries” than Chime. Much of that growth came not from new accounts, but from relaxing their definition of Primary towards Chime’s generous standard. As I recall, changing the standard nearly tripled Cash App Primaries overnight.

Cash App Actives (not primaries) grew by only 1M in this period up to 59M, which is 6x Chime Actives. Cash App recruits Actives through P2P, then cross-sells the debit card, and finally tries for Primary.

The other odd outcome is ARPAM. Chime mentions increasing engagement in a number of places, but ARPAM grew only 5% YoY and was essentially flat intra-year. Further, all revenue sources benefit from an inflation tailwind of 2.7%. So where is the lift from multi-product customers? It would seem to add only ~2.3% to ARPAM (5% growth less 2.7% CPI).

The only explanation I can think of is that “AM” (Active Members) is outgrowing PAMs (Primary Active Members). That would increase the denominator without increasing the numerator. As we will see, most of the growth products depend on Primaries. Advice to Chime: Disclose Primaries and calculate ARPPAM!

Efficiency ratio

Chime keep reminding us they are not a bank, but become more bank-like all the time. Therefore, using Efficiency Ratio as an expense metric is increasingly warranted.

Efficiency Ratio (ER) is calculated as Non-Interest Expense over Net Interest Income plus Non-Interest Income. It measures how effectively a bank turns expenses into revenue. Chartered banks target an ER in the 50-60% range, although some narrow banks can get below 40%. ER depends to a degree on business mix.

Chime has a chart on page 19 of the Earnings Supplement that gets to the same idea but calculates it differently. Their denominator is “Revenue” rather than Gross Profit or Transaction Profit, two other metrics they report. The difference among these three is that Gross Profit and Transaction Profit eliminate contras against revenue whereas page 19 ignores all those contras. Here are Chime’s own definitions:

Gross Profit is defined as Revenue less Cost of Revenue

Transaction Profit is defined as Gross Profit less Transaction & Risk Losses

Page 19 excludes “Cost of Revenue” and “Transaction & Risk Losses” as if they are not real expenses. They are. Chime should net them against the denominator or add them to the numerator. I calculated ER with Chime’s own metrics that treat these expenses as contras. The numerator is always Chime’s non-GAAP Opex:

Even using Revenue, Chime is above best practice ER. Using the more realistic metrics puts them increasingly far away. Chime’s numerator is also non-GAAP expense where a bank would use GAAP, making Chime’s ER even worse.

Effectively Chime’s treats contras as expenses except when measuring efficiency. Since the company lost money in 2025, any reader that took accounting 101 would expect expenses are higher than revenue, so why do they show this metric as evidence of improving economics?

As it happens, the most rigorous metric shows the best improvement. The Revenue metric ends flat versus Q1 and only declined 2% QoQ. The Transaction Profit metric is 6% less than Q1 and 5% less QoQ. It demonstrates operating leverage better!

Areas that demonstrate real progress

Chime made real progress on Q4 revenue metrics that aren’t confounded by favorable definitions.

Payment’s revenue growth

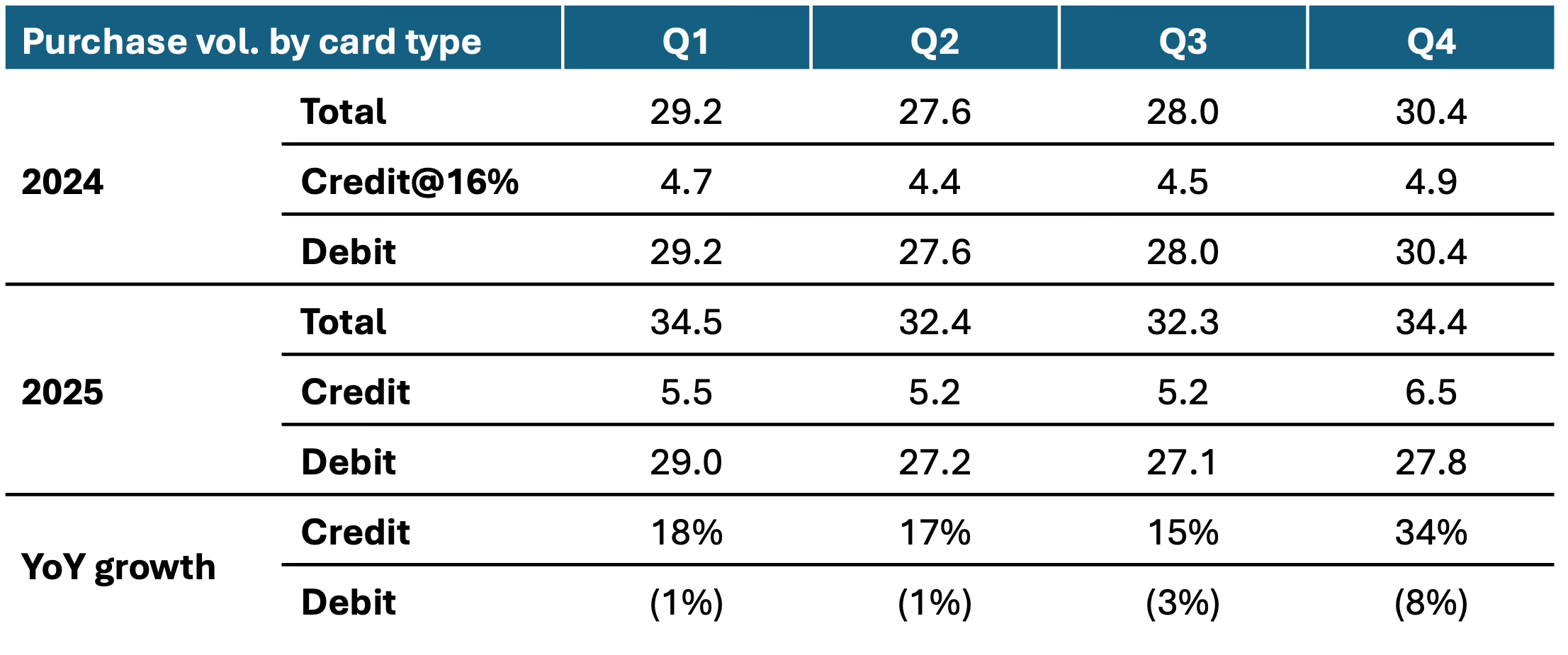

Chime purchase volume growth was higher than 2024, but effectively flat intra-year.

Chime did not disclose 2024 Credit volume but the first three quarters of 2025 all came in at 16% of Purchase Volume so I assumed that rate for full-year 2024. They clearly cannibalized Debit Volume to build Credit volume.

The rewards Chime Card was only introduced in Q3. Chime disclosed that Chime Card earns ~2x the interchange (IC) of their debit card. Therefore, the decline of debit spend is a favorable outcome since it shifted to the higher-IC Chime Card (credit).

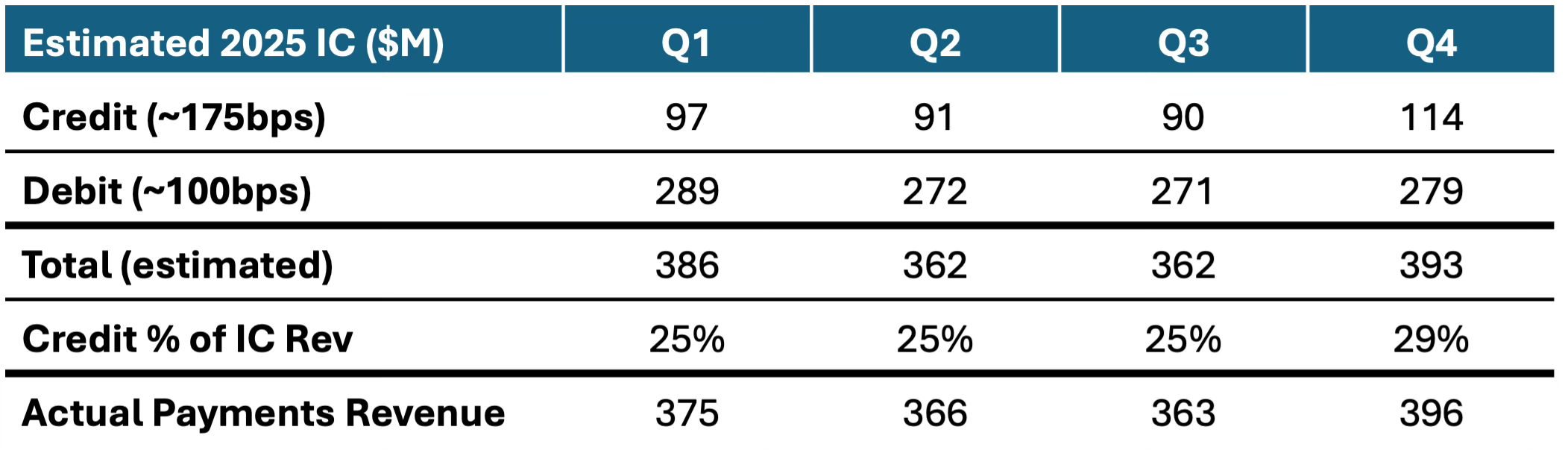

This shift had clear revenue impact in Q4: Chime Card generates ~1.75% IC while the debit card generates ~ 1.0%. That produces the following estimated 2025 revenue:

The Chime Card pays rewards, but limits those rewards to 1.5% on a single category. Unless customers optimize spend on that category, the trade-off is positive. Chime Card rewards were new in Q4 and costs are not disclosed. Those costs are likely in Sales & Marketing expense which grew $10M in Q4 QoQ whereas they were flat in Q4 2024. If that $10M is rewards cost, the net impact on revenue is still positive, although less so.

The Merchant Settlement may be a headwind. The settlement caps interchange on “Standard” cards at 125bps, 50bps below the Chime Card average. In Q4 alone, that cap would reduce IC by $33M, or 10% of total IC revenue. Further, if Rewards costs are netted against IC, the net IC for the Chime Card could drop below debit IC. Rewards costs cannot exceed 25bps of spend under the cap – which is not very appealing to cardholders. The settlement is before a judge and may not go forward in its current form. Some big merchants oppose it for not going far enough.

Moving cardholders from Debit to Chime Card will continue to work unless the Settlement Cap happens. Congratulations are in order.

Lending revenue growth

Chime has two lending products:

MyPay, an EWA-style advance on direct deposit

Instant Loans, an installment loan similar to Affirm or Cash App Borrow

Instant Loans

Instant Loans are relatively new with limited disclosures. Here is everything Chime says about the product in its Investor Presentation:

I may have found evidence of the product in Bancorp Bank’s Call Reports. If that item was Instant Loans, they had a big Q1 launch and then settled down to steady state at half the launch rate. Bancorp reported $169M of such loans, which is close enough to half of $400 that I now think the other half is at Stride bank, but not disclosed by Stride. We can estimate the average loan size as follows:

10% of 9.5M Actives suggests 950K loans outstanding

The loans have a tenure of 3 months, and the Bancorp Call Report detailed ~$40M of Q4 volume. Multiply by 2 to add in Stride’s volume to get $80M of Q4 balances

Dividing the $80M by 950K loans yields $84 average outstanding

Since each loan has 3 payments, we need to increase that to $127 (i.e., one-third have 100% outstanding, one-third have 66% outstanding and one third have 33% outstanding)

$127 is at the low end of the $100-500 Instant Loan borrowing limit. It is 20% higher than the average industry-wide EWA ($106). The math is believable to me.

The Addressable market is Primary Accounts given the qualification requirements, but primaries are not disclosed in the earnings release. In 2025, a Chime executive said two-thirds of Actives were Primary – yielding 6.4M primaries. 10% of Actives would be 950K borrowers. That means penetration is already 15% of the addressable population (950K/6.5M). Astonishing in such a short time. This population is clearly hungry for credit and Instant Loans meets that need despite the 29.7% APR.

I noted in my Klarna post that Klarna and Affirm both offered similar products with APRs ranging from 0-35%. Chime Instant Loans are always 29.7% whereas the other two products offer a lower APR to better credits. The availability of alternatives at lower rates could lead to adverse selection into the Chime product. Chime must believe the convenience of bundling offsets their higher rate for good credits.

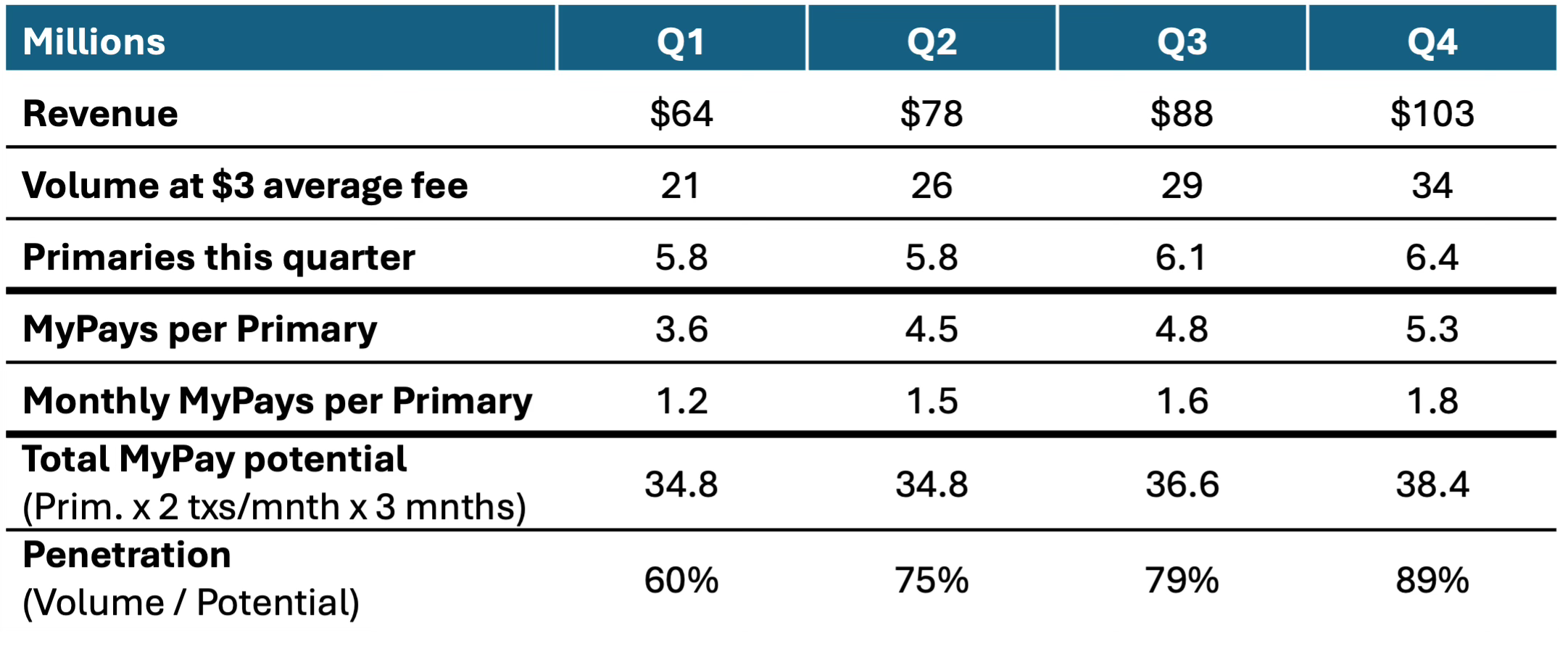

MyPay

MyPay is not a loan, but an advance against the customer’s direct deposit. While the actual qualification terms are more complex, the product is effectively restricted to Primaries. Like other EWA products, Chime charges no interest but instead offers an optional Instant Advance. They charge 3% of face value for an instant advance, with a $2 floor and a $5 cap. ACH advances are free, but take 1-2 days.

For the market average advance of $106, a MyPay customer pays ~$3. According to CFPB research 90%+ of EWA users pay an instant fee similar to Chime’s. Assuming the average advance yields $3, usage is remarkable, and likely fully penetrated:

MyPay was only introduced in 2024, making these estimated penetration rates remarkable. Congratulations are due. I am a believer in products like EWA and BNPL that provide modest credit to low-FICO borrowers at zero interest. I am flummoxed that some activists oppose them.

That leaves Chime with two challenges: Can MyPay be profitable and where is the growth going to come from given the already high penetration? For the first question, Chime provides actual data. Loss rates have steadily declined to today’s 1%. Of course, to do this, Chime had to tighten underwriting standards, shrinking their addressable market.

Put another way, if MyPay already captures 89% of primaries and some of the remaining 11% can’t be underwritten, where is the growth headroom? Some of their clients won’t even need the product because they have higher incomes. Indeed, growth rates had dropped as low as 12% QoQ between Q2 & Q3 before Q4 recovered to 17%. Some of the Q4 growth came from rising primaries due to tax season (according to the company). Usage could also increase if users take MyPays more than once per pay period. Of course, all my assumptions and math could also be wrong.

The better strategy is growing Primaries. Given the high penetration, the bulk of new primaries will use both the Chime Card for higher payments revenue and MyPay for higher lending revenue. Chime detailed two initiatives to raise primaries:

Chime Enterprise, a bank at work program with MyPay at its center

Chime Prime, a premium tier account requiring $3K in monthly direct deposits paying 5% cash back on one spend category. And airport lounge access!

Chime Enterprise is spot on. if Chime signs employers with lots of Chime-relevant employees it gets new Primaries at very low CAC. I am skeptical of Chime Prime as many of those consumers can get free checking at any bank. The 5% is also not sustainable if too many customers are optimizers. I also suspect that many who qualify for Chime Prime won’t use MyPay at high frequency.

MyPay may be so successful it is running out of headroom. Further growth relies on expanding Primaries, which faces competition from Cash App and others. Chime Enterprise is a sound strategy to address this.

Conclusions

I started this post expecting to reinforce the pessimistic view I presented for Q3. I surprised myself by coming away more positive. I still think Chime ought to fix all the metrics confusion that masks profitability. And it would be nice to see actual profits! They claim profits will appear in Q1. We’ll see.

On the positive side:

The Chime Card genuinely increases revenue without increasing risk; It has lots of headroom given only 21% penetration today. It’s faces an existential risk if the merchant settlement goes through, but that is a big if

MyPay & Instant Loans have tapped into an insatiable demand for short-term credit in the Chime demographic:

MyPay may be nearing terminal penetration of the base, although Chime Enterprise may expand that base

Instant Loans grew despite lots of competition and very high APRs. Risk constraints may limit growth (longer terms, higher tickets)

Despite the success of these products, ARPAM only rose 5% YoY and declined for Q2 & Q3. That doesn’t make sense unless Actives outgrew Primaries

The key for Chime is growing Primaries. These provide a low-CAC base to cross-sell Chime Card and the Lending products. Actives growth has too much seasonality to predict. Q1 typically shows growth, but Q2 & Q3 slow down. Primaries are not reported but should be.

If the history holds, the seasonal Q1 growth spurt may deliver the Q1 profit guidance, but slower growth in Q2 & Q3 could return to losses. Can Chime break the pattern?