Key insights in this post

X announced a new P2P service as the first product in its X Money Suite, a Super App expect to offer many financial services

The P2P service operates on the stored-value model that uses Visa Direct to move funds in and out of the “X Wallet”; this is similar to Venmo & Cash App

Neither the P2P service nor the Super App are likely to win in the US

In P2P, X is not likely to get much traction off-X

Stored value services are losing to Zelle, which operates real time from your checking account and is embedded in the bank app you already have

The X service would allow X readers to tip or subscribe to X writers, but that is a modest-sized use case

Visa Direct can be expensive when senders only fund discrete payments rather than creating a balance to fund many payments

Super Apps emphasize convenience over choice, while Americans prefer choice

Super Apps work in China where the government puts too many controls on App Stores

They have not worked in the US where App Stores provide a plethora of choice — both for financial services and services that compare financial products

X Money could not be best-in-breed in every financial vertical as many of them are APR/APY or performance driven, not convenience-driven

Incumbent & insurgent financial services providers are also trying to diversify across financial verticals, with limited track record of success

X Money might become an advisor on financial services rather than a provider of those services

Become an all-in comparison site, similar to Bank Rate or Credit Karma

Become a personal financial management (PFM) provider that helps consumers manage their fragmented financial holdings

Introduction

I had a different article written for this week, but pushed that to next week so I can publish on this development in a timely fashion.

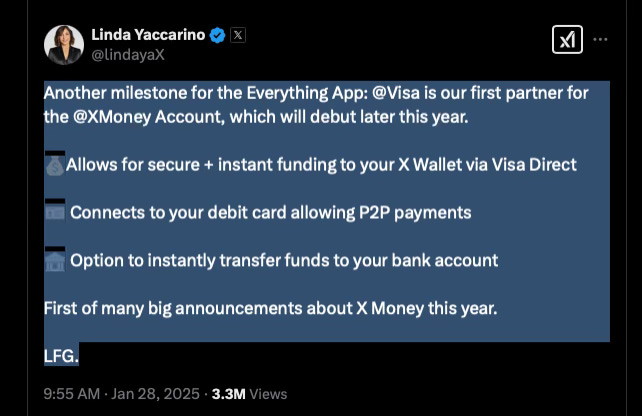

For those of you paying attention, X announced a partnership with Visa to launch a new P2P service. It would use Visa Direct to move money and leverage the dense social relationships on X to build a customer base. The P2P service is being positioned as an onramp into an X-branded “Super App”, called “X Money”, that will offer a portfolio of financial services.

Appropriately, the formal announcement was on X:

There is room in the market for a P2P proposition that allows X readers to pay X writers – that is well-trod ground. But I am unconvinced that X can win as a general purpose P2P. And I have never been a believer in “Super Apps” for the U.S. market.

For the removal of doubt, I am apolitical and have never been active on X. I lease a Tesla, and I think Space X is one of the greatest technology developments of my generation. My Tesla even has Space X floor mats. Plus, The Boring Company has the punniest name ever. So I don’t underestimate Elon in any technology arena.

But as my readers know, I was there at the founding of Zelle and have followed developments in P2P ever since. I wrote about this a few weeks ago in my post on Apple Pay vs. PayPal. So, I have informed views on these topics. This post will discuss the barriers to both new P2P services and Super Apps to justify my skepticism.

Incumbent P2P services are hard to displace

The market already has five material P2P services, but Zelle is the leader and its share is growing. The others are Venmo, PayPal wallet, Cash App, & Apple Pay Cash. Google and Facebook both had services but shut them down. Others have tried and failed.

For the record, Zelle’s most recent data show it is bigger than the others combined on most dimensions and growing faster. Zelle is growing 25-30% YoY depending on the metric. PayPal Wallet reports its YoY P2P TPV grew 5% as of Q3. Venmo grew 8% YoY in the same period. Cash App grew inflows by ~13%%. Apple Pay Cash does not report metrics, but is the smallest of the bunch not least because it doesn’t support transfers to Android users. None of these figures are inflation adjusted, so transaction growth is likely lower.

New P2P services face barriers to entry only some of which can be addressed by X:

Ubiquity. Both the sender and the receiver have to be enrolled. The first outbound payment can serve as the invitation, but there is no guarantee that the receiver will become active as a consequence.

X has a lot of users, but is not as broadly used as Facebook or Google, and both those services failed. Venmo & Cash App grew through virality, but the bulk of that growth was before Zelle showed up in everyone’s bank App. Growth slowed in the aftermath.

Revenue model. Zelle has no revenue model. It’s purpose is digital engagement with the user’s primary DDA bank and to displace cash and checks. That makes it tough to compete with. P2P at Venmo & Cash App are free, but they monetize elsewhere:

By issuing a debit card to pay down any balance

By charging extra to move any balance back to your checking account

By getting users to spend balances in eCommerce where the merchant pays an MDR

The X announcement does mention a debit card, which earns interchange, but only if people use it. The X writers are the likely payees who will build balances — but some sources claim this group is only 10% of X users. My bet is those writers are already banked, so why not transfer funds back to their bank where they already have a debit card? Or transfer the money back and then spend on their Credit Cards – which earn rewards.

The only reason to use an X-branded debit card is if X follows the Venmo/Cash App route and charges 1% of face value for real-time transfer – which is noted as an option in the announcement. In that case, the user can save money by spending down their balance on the debit card.

X might also charge writers a processing fee for subscription services. I am writing this post on Substack which uses Stripe for this purpose. If I ever introduce a subscription tier I will be using Stripe – who charge ~3% while Substack takes 10%. X might put a similar arrangement in place. The question is whether that generates sufficient traction for readers to use X-P2P for anything off-X. I suspect not.

X P2P may just monetize by engagement on the Super App, i.e, X Money. Users become part of the X Money CRM for direct marketing. So, X P2P might serve to lower CAC for X Money. Well worth it if it works. But none of the Super App’s other services have been announced, so, initially, the P2P service is not likely to be a profit-spinner.

Cost Structure. Not that past is prologue, but the two failed services – Google & Facebook – were both social networks that based their P2P on Visa Direct. Zelle settles between banks via ACH and Cash App and Venmo are both stored-value services that move the money on-us, i.e., via a book transfer from one stored value account to another. So, the P2P clearing and settlement costs on Zelle, Venmo, & Cash App are very low.

All these services use Visa Direct for some purposes. Zelle uses it to reach consumers that don’t bank with a Zelle member (under 5% of volume). Venmo & Cash App use Visa Direct to move money back to a consumer’s bank account in real time, for a fee. Apple Pay Cash uses it for various purposes as well. But none of them use it for routine P2Ps.The standard rates (interchange plus network fee) for Visa Directs are roughly 25 cents for the inbound (AFT) transaction from a bank account and about 12 cents for the outbound (OCT) transaction to a bank account. Since X Wallet seems to be a stored-value service like Venmo or Cash App, the AFT fee is only incurred when the send account is funded and the OCT is only incurred when the recipient wants to move the money to their bank account in real time. P2Ps are no-cost book transfers from one X Wallet to another — just like Venmo & Cash App.

However, if most of the volume is readers paying writers, most of the reader transactions will incur an expensive AFT. And if the writers want to actually use their funds they will want it back in their bank account; other services offer the choice of a free ACH or a Visa Direct OCT with a 1% fee.

The economics only work if readers overfund their X Wallets so they have a slush fund to tip writers ad hoc. Think of this like EasyPass or the Starbucks App. The same incentives apply. On the writer side, the economics only work if the writers use the X debit card to buy down their balance or writers always opt for the real-time fee back to the writer’s DDA. If readers fund each discrete transfer rather than holding a balance and the writers use ACH to concentrate their earnings in their bank account, the economics are underwater.

Visa has been known to discount Visa Direct interchange for new use cases. Generally, such discounts are time limited. In effect, such discounts would tax the banks to subsidize the X P2P service which competes with Zelle. It would be a difficult conversation, but not unprecedented.

Conclusions on X P2P

A few weeks ago I outlined the criteria for success in digital wallets.

Have a big customer base

Have a way to monetize

Have a Home Field with a compelling use case

X has all of these: X has a big customer base, debit cards and instant transfers are a way to monetize, and readers paying writers could be the home field use case.

However, I think engagement is too weak to wean users off the incumbent P2Ps & Cards for routine transactions. X does have a lot of users, but almost all of them have bank accounts that come with Zelle -- or they independently choose Venmo or Cash App. Readers paying writers is a strong use case, but happens only a fraction of the time.

For example, Substack is estimated to have made $30M in 2024 revenue from its 3M subscribers out of a 20M user base. So $100 per year per subscriber, but only 15% actually subscribe. Many Substack writers use X to promote their Substack posts, but they might just monetize on Substack. Every time I publish a post, Substack encourages me to promote on X with standard templates provided.

Even if lots of readers tip their favorite writers, those writers seem unlikely to use the X debit card. Writers likely have a bank-issued debit card already, and I would bet the vast bulk of them have rewards credit cards as well. The only reason to use the X Debit Card would be to avoid real-time fees, but those are avoidable by using ACH and waiting a day or two. The real-time option is popular on Venmo & Cash App, but those populations are young and many are cash flow challenged. My guess is the X writers that attract big readership have day jobs to pay the bills and a day or two delay in collecting their X revenue doesn’t really impact their life style.

My conclusion is that X P2P may attract modest volume but is unlikely to extend to any off-X use cases. The incumbents don’t have a lot to worry about. But can P2P be an effective on-ramp to other Super App financial offerings?

Super Apps don’t work in the US

Super Apps were all the rage 10 years ago when Alipay and WeChat were scaling in China. Both solutions offered an array of curated functionality that interoperated seamlessly. And both offered Payment Functionality. Alipay eventually became Ant Financial which offered investments, deposits, loans and insurance. WeChat built out its own portfolio of services.

Expert opinion claimed Super Apps were coming to America. Super App fever was at its height when I was at JPM. Our management team took a trip to China and came back convinced. I was a skeptic; of course, I am a skeptic about everything, and occasionally that skepticism is justified. This is one of those times.

I remember being interviewed at an investors conference back then (circa 2018?) when someone in the audience rather belligerently suggested that banks were toast because Super Apps were coming to America to sweep the field. I disagreed with the following argument:

In China, App Stores were not as big a phenomenon because of government controls and other limitations. Instead, a few giants curated an integrated experience into a single App with good-enough functionality in each use case

In the West, we had open App stores with thousands of Apps – often dozens in each use case. Here, it was all about choice. It would be hard to build a Super App that had best of breed in every use case and still serve every segment – Americans instead curated their own best-of-breed suite via App Stores. However, those apps would not interoperate as they did in China

So, it came down to choice versus integration. In China, integration won, in the U.S., choice won. I don’t think we are going back from here. To make a Super App attractive, X would need to be best of breed in every vertical. For financial services that would mean deposits, lending, wealth, and insurance. This is unlikely:

In deposits, Checking is convenience-based & Savings is price-based:

In Checking, most accounts are free above a $1,500 minimum balance and consumers still pick largely by the physical proximity of a branch network. If checking is free, why switch to a Super App checking account with no local branches or ATMs? The super App could partner with a single national bank, but any proximate consumer could open those accounts anyway, so why do it on X?

In Savings, APY rules. Consumers happily go online to search out the highest rates, no matter how small or obscure the bank. Deposit Insurance makes this safe. But how could a Super App always have the top APY without consequence to their own economics?

In lending, APR drives most decisions, although card rewards matter more for affluent consumers:

In Mortgages, consumers want the lowest APR given the size of the loan. Those rates are underpinned by the GSEs so it is hard to be too low and still participate in the secondary markets. If you can’t use the GSEs you likely need a balance sheet to hold the loans. X doesn’t have one

In auto loans, the OEMs often subsidize the APRs, so no matter how low an independent lender’s APR, the Acceptance Companies will likely be lower. Banks are more competitive in used cars where there are no OEM subsidies, but it would still be hard for a Super App to always have the lowest rate

In Credit Cards, APRs and line size matter, but rewards are a key source of differentiation. Cash back rewards are commoditized, but cobrand rewards are hard to replicate. For example, there is only one Amazon Prime Rewards Visa card with 5% cash back on Amazon. No one will take a generic card just because it is bundled in the Super App. X has no rewards currency of its own to differentiate. X could channel rewards cash into a tip fund for each cardholder that can then be used to pay writers, but is that salient enough compared to, say, Frequent Flyer miles?

In Investments, some are not subject to provider choice (401Ks) and most others are sold on performance, which is hard to consistently deliver best-in-class

In Insurance, state level regulation makes it hard to deliver a national proposition with guaranteed best-in-class features and pricing

In other words, the Super App will almost never have the best proposition on every product at the same time. Consumers will do better shopping within each category than relying on the Super App. Entire industries help consumers find the best deals, from savings rates (e.g., BankRate.com), to credit cards offers (e.g., Credit Karma), Auto Loans (e.g., Lending Tree), every type of insurance (independent agents and Apps), mortgage rates (Mortgage brokers) and investment firms. Those services typically use objective criteria, and convenience is not one of them.

Just ask the typical regional bank how many DDA customers use their credit cards or investment services. For credit cards, the penetration is usually around 10% and they start from a primary DDA not a small stored value account. The big issuers do better, but some of that is not true cross-sell but cobrand. Even the biggest banks, like JPM, BAC, and WFC rarely get the full wallet from their affluent customers.

Some Fintechs are trying the same share of wallet strategy starting from either lending (SoFi) or investments (Betterment, Wealthfront, etc.). Amex, Synchrony, Discover, and Ally have all had limited success selling DDA from a lending entry point. Schwab has done better from an investment entry point. Arguably, USAA has reasonable success across all products, but they have a strong affinity that X lacks.

Both Venmo & Cash App are trying to diversify in similar ways, but with limited reported success. They both have debit cards, but only Cash App’s seems highly used – and that is because Cash App has a big underbanked customer base. Few banked consumer have any reason to use a P2P-issued debit card.

Conclusion on the X Money Super App

There is no reason to believe that the X Money account can displace incumbents or insurgents. X Money may be more convenient for some active X users, but almost all those users already have all these products and presumably chose them for a reason. There is no reason to switch in evidence yet.

Overall Conclusions

The X P2P service can be successful in the narrow use case of transmitting tips and subscriptions from X readers to X writers. Other payments companies have succeeded at that on other writing platforms – like the Substack platform you are on now. I can’t think of another on-X use case that needs to move money and I can’t imagine users of the 5 incumbent P2Ps would switch to X-P2P for off-X payments. There is simply no reason to do so – particularly as Zelle doesn’t require a separate stored value account and provides real-time transfer into the checking account for free.

Super Apps have never worked in the U.S. They are the digital equivalent of the “financial services supermarket” concept that never worked in analog. Many banks and Fintechs today are also pursuing share-of-wallet strategies based on stronger attachment points than X – with modest success. Whole industries help consumers unbundle their financial services to best-in-breed providers – where best-in-breed usually means lowest APR, highest APY, lowest fees, or highest returns. Re-bundling is unlikely to appeal.

X Money could become a marketplace, more like Credit Karma or Bank Rate. X Money could help consumers find the best deals rather than offering proprietary products. It could then aggregate the back-end reporting from those unbundled providers to deliver a PFM-type experience. Open Banking makes this easier today.

This plays to X’s strengths as the Affiliate Fees it earns would be similar to the advertising revenue it earns for core X. It leverages the first-party information on the customer base without the overheads of delivering financial services. It could leverage AI to help with product selection and financial management – after all, AI is something Team X likely knows more about than most financial institutions.

That subheader is one for the ages