Can PayPal turn it around?

Their Strategy doesn't address the market headwinds

Key Insights in this post

PayPal reported disappointing 2025 earnings and discouraging 2026 guidance as the key PayPal wallet product showed slow growth

PayPal’s historical role in providing trust and reducing POS friction has been commoditized:

eCommerce merchants have established direct trust either as independent entities (e.g., Amazon) or by aggregating small merchants (e.g., Shopify)

Many of these household names have their own payments solutions that deliver low friction and high security (e.g., Amazon One-Click, Shop Pay)

Independent wallets like Apple Pay, Google Pay, Link and Paze compete for the limited open space outside walled gardens

New payment methods (Stablecoins in x-border, A2A domestically) could erode growth potential outside the core Retail e-Commerce vertical

PayPal’s investor presentation did not present a convincing “Win Checkout” plan to restore Wallet growth even though Wallet accounts for most PayPal revenue

The other four strategic initiatives were either nice-to-haves or irrelevant to near term performance

“Scale Omni & Grow Venmo” add TPV and Revenue but not earnings

“Scale Omni” is all about Debit; PayPal & Venmo debit cards are growing only by paying economically unsustainable rewards

“Grow Venmo” focuses on a brand that produces only 5% of revenue and is losing share to Zelle. Most TPV growth is zero-revenue P2P

“Drive PSP Profitability” sacrificed TPV growth for earnings, but contributes a fraction of corporate profitability

Enterprise Payments/Braintree is a distant 3rd or 4th to market leaders Stripe & Adyen. GPN/Worldpay also has material share

The new VAS they highlight are features that the market leaders have offered for years, while those leaders push the frontier

I would divest this unit as it doesn’t contribute to “Win Checkout”

“Transaction Loss Impact” is a worthy effort, but not material. It may be an artifact of rising Debit TPV, which has low fraud due to EMV

“Scale Next Gen Growth Vectors” are nascent. Even if successful, they won’t contribute to earnings or TPV any time soon

“Win Checkout” needs a new proposition

Trust & Friction have been commoditized, but PayPal’s straegy focuses only on improving experience and better marketing. That is more of the same.

Getting to the POS might be possible, but is not differentiating

The Debit efforts are likely producing profitless TPV growth

Accessing Apple’s NFC chip might help, but consumers would need a good reason to use PayPal NFC instead of Apple Pay. There is none

The only new proposition I can think of is superior “offers”, i.e., Honey 2.0:

Get merchants to share SKU in return for MDR discounts on successful conversions

Use SKU to tap CPG promotional spend so that PayPal itself doesn’t subsidize the offers as it does for debit rewards

Position on merchant product pages to present SKU-level offers (like BNPL providers do), which might also improve lending conversion

Require A2A wallet funding to complete offer transactions, offsetting lower MDR with lower funding costs

Conclusions

PayPal’s legacy value proposition is commoditized and its SAM is shrinking

Something fundamental has to change to restore growth, but nothing fundamental is outlined in PayPal’s strategic initiatives

The “offers” model I outline is extremely difficult to execute and may be completely impractical

Unless some alternative proposition emerges, growth is unlikely to return

Introduction

I keep wanting to leave PayPal be, and then they make news. In case you didn’t notice, PayPal reported disappointing 2025 earnings and discouraging 2026 guidance. That led to a CEO shift. The stock dropped almost 20% in response, and is down ~50% in the last 12 months.

Financials aside, is this a result of poor strategy, poor execution on the right strategy, or market shifts. I think it is mostly market shifts. If I’m correct, new leadership won’t be able to change the trajectory much without fundamental change They can’t clear away those pesky market obstacles to the current model.

I have written about many of these obstacles in prior posts, so some of my commentary will be familiar to tenured readers; I will try to anchor to their recent disclosures to keep things fresh.

What happened to PayPal’s historical moats?

PayPal was originally a key lubricant for eCommerce growth. Early eCommerce was perceived to be unsafe; many merchants were new and small and consumers didn’t trust that their card data would be safe. Most merchants also didn’t store card data, so the consumer had to re-enter it every time, creating friction.

PayPal reduced all. PayPal itself stored payment credentials with password protection – the consumer didn’t have to trust the merchant so long as they trusted PayPal. And most online merchants accepted PayPal because it reduced cart abandonment. PayPal mostly solved the trust problem.

PayPal also funded accounts via ACH in its early days. That allowed it to charge merchants less than Cards. Everybody won except the card issuers.

Today, most of those eCommerce obstacles have been solved in other ways.

Merchant Trust. The trust problem has been solved on two dimensions:

Amazon, Walmart and other household names now capture 60%+ of volume. They are perceived as safe without other security measures

Smaller merchants migrated from standalone web-sites to either marketplaces (e.g., Amazon, Ebay, Etsy) or Platforms (e.g., Shopify). Effectively those large intermediaries make smaller merchants safe to do business with

Card-on-file and tokenization. The biggest merchants, with recurring activity, store consumers’ card credentials and shipping data. The card numbers are exchanged for Network Tokens so even if the merchant is breached, the consumer’s data is safe. Card-on-file removes checkout friction even more than PayPal does. It is no mystery why Amazon doesn’t accept PayPal – its customers don’t need it!

Ubiquity. PayPal is still the most widely accepted digital wallet, but it now has localized competition in key venues: Apple Pay is king in-app. Shop Pay is favored on Shopify where most small merchants have stores, Link serves Stripe customers, and Paze is trying to become the third-party alternative

ACH funding. The networks convinced PayPal not to steer to ACH. As a result, PayPal’s accounts are mostly funded by cards. That reduces PayPal margins although it also reduces fraud and operations expense. Today, independent A2A providers leverage Open Banking and ACH to underprice both cards and PayPal

Global footprint. PayPal followed many of its early merchants as they globalized. It may even have higher share outside North America; but, competition has emerged in many key countries, both from local wallets and A2A methods

A critical event was the spin-out of PayPal from eBay. PayPal was the default payment method and gateway for small merchants because those merchants faced the highest trust barriers. Many small merchants started with PayPal on-eBay, then took PayPal with them to their standalone stores. After the spin-out, eBay established its own payment methods, diminishing PayPal’s flywheel.

Today, most small merchants start on Shopify, defaulting to Shopify Payments and Shop Pay. PayPal is available as a payment method, but is rarely used as a gateway. Amazon Marketplace displaced eBay as the second channel for small sellers, so a portion of small merchant volume processes on Amazon Payments even if the core store is standalone.

The major obstacle has always been Point-of-Sale. PayPal tried repeatedly to get a POS presence, with limited traction. The wallet was cut off from ~80% of spend. Today, they are trying again with their Debit Card strategy, but I will show that this is a tough slog.

Summary of the obstacles

Most of the trust & safety issues that PayPal solved at the dawn of eCommerce now have other solutions:

Concentration of eCommerce into high-trust venues has reduced the need for a trustworthy third party

Other wallets leverage large consumer bases and/or merchant bases; those wallets often get better positioning within a walled garden

ACH funding is less of an advantage as PayPal’s steering tactics were softened and most consumers preferred to fund with cards to capture rewards

PayPal still has a “global” advantage, but that is eroding as well.

Does PayPal’s strategy build new moats?

PayPal’s Q4 25 earnings presentation quantifies the outcome of these headwinds:

Modest YoY growth mostly came from low-revenue Venmo

Active Accounts grew only 1%

Monthly Active Accounts grew 2%

Engagement grew 5% (transactions per account)

A material portion of volume growth is from Debit Cards rather than Wallet spend

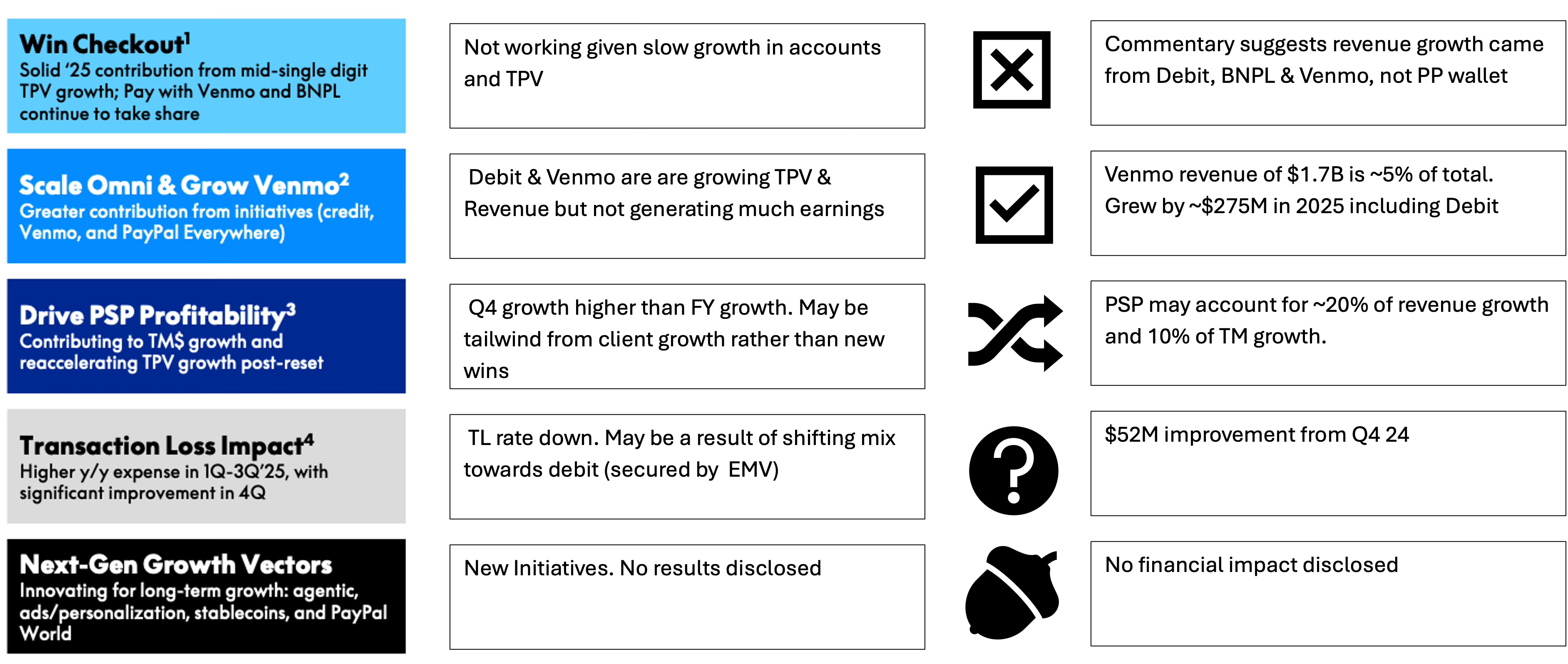

PayPal outlines 5 strategic initiatives to restore growth (up from 4 last year).

They have not succeeded in “Win Checkout”, which accounts for the bulk of revenue and profit. They have grown Venmo, but Venmo is still a small revenue contributor and faces competitive headwinds of its own. Critically, Venmo profits are not disclosed. The other three are worthy, but marginal to performance.

I will first show why the last four can’t make up for any shortfalls in “Win Checkout”, then deal with “Win checkout”

Scale Omni & Grow Venmo (Discussed on Page 6)

The page focuses on lot on TPV growth and very little on revenue or earnings:

Scale Omni

Omni = Debit. PayPal repeatedly tried to tap into the 70-80% of commerce that is CP, but those attempts failed. PayPal & Venmo now issue branded debit cards to facilitate CP commerce. That generated $35B of global TPV, most of which is in the US. The page discusses no other “Omni” Initiative.

Of course, every PayPal customer already has a bank-issued debit card. To change behavior, PayPal customers need a good reason to use the PayPal or Venmo debit card – and they have one: Rewards. However, exempt debit interchange can’t fund generous rewards. Debit clusters in everyday-spend verticals, where share concentrates in large merchants. Those merchants get lower exempt interchange from routing negotiations.

PayPal doesn’t expose the revenue or expense from their debit programs, but the net cannot be high. The Fed’s debit survey showed that in-person exempt debit transactions average ~30¢ interchange on an average ticket of $40. That is 75bps of revenue from which to pay rewards:

Venmo cards pay 100bps of rewards, suggesting they lose 25bps per transaction

PayPal cards earn 5% on one category. If optimizers concentrate spend in the 5% category, losses are huge. I just got off the phone with a colleague who does just that in Grocery. Pure coincidence, but the behavior may be common

CNP transactions have both higher interchange and higher ticket size, but PayPal wants consumers to pay with the wallet online, not the debit card. Using the debit card online, outside the wallet, may destroy value if IC is lower than wallet MDR

PayPal does not expose rewards costs. The ~$300M jump in 2025 YoY Sales & Marketing costs may reflect the 40% jump in YoY debit TPV. All other Opex categories were flat to down.

Finally, If PayPal gets its ILC charter, it will quickly exceed the $10B Durbin threshold due to lending volumes. Regulated IC is nominally half exempt IC. PayPal could try to keep using a third-party issuer but, as a Durbin-regulated entity, that may count as “circumvention” under Durbin rules – a no-no. So the charter strategy may be incompatible with the debit strategy.

While Omni/Debit is growing TPV faster than PayPal wallet, its profit contribution is likely modest or negative. PayPal doesn’t disclose enough data to know for sure.

Grow Venmo

Venmo TPV grew faster than PayPal TPV, however, Venmo TPV growth also includes Venmo Debit which is effectively double-counted in the Omni column. As discussed above, Venmo debit likely has thin or negative margins due to rewards costs.

Venmo has much higher engagement than PayPal wallet, at ~3 transactions per month. Venmo MAAs are ~30% of overall MAAs, and grew 7%. Venmo transactions grew 9% per account. Given all Venmo accounts are in the US, Venmo, may account for more than half of US transactions.

Unfortunately, most Venmo TPV is P2P which generates no revenue at all. Venmo generates only 5% of company revenue despite accounting for 18% of TPV. That is revenue, not profit.

Attempts to turn Venmo into a general-purpose wallet, have shown underwhelming results: In the 2025 Investor Day presentation, Pay with Venmo was reported to have $8B in 2024 TPV, with management projecting a 40% CAGR through 2027. Therefore, we should have seen ~$11B of TPV in 2025. Management has not disclosed the 2025 result, suggested they are not proud of it. Either way, US “Branded” TPV may be ~$200B+, so Pay-with-Venmo is a rounding error.

Despite its growth, Venmo lost share to Zelle. Venmo TPV grew 12% YoY, including debit. The last time Zelle published data (for H1 2025), TPV was growing at 25% YoY, excluding debit. Zelle TPV is 3x Venmo and growing twice as fast. Venmo has high growth relative to PayPal wallet, but is still losing share in its core market.

Conclusions on Omni & Venmo

These are both growing TPV faster than PayPal wallet, but from a modest base. Earnings growth is not disclosed and may be less impressive. Highlighting these areas for their TPV growth is understandable, but it doesn’t solve top-line or bottom-line challenges. the Initiatives do nothing to address the wallet headwinds.

Drive PSP profitability (Page 7)

PSP (a.k.a., Enterprise Payments, Braintree) accounts for 44% of TPV but only a fraction of revenue or profit. Most clients are enterprise-class where the pricing norm is a flat fee per transaction that may be under 1¢.

Growth slowed after PayPal raised prices in recent years. Higher prices restored profitability from the clients that stuck around, but it likely slowed new wins. Most of the reported growth is likely same-store sales for long-term customers. Page 7 shows no strategy that might improve the win rate.

Page 7 lists a series of value-added services that are useful, but years behind the competition. For example, “authorization optimization” is something Adyen pioneered over 10 years ago. Omnichannel is also something the competition already does. Payouts are offered by Adyen & Stripe and by specialists like Payoneer. These VAS are useful cross-sells, but not differentiating.

Enterprise Payments is an also-ran in a sector where it was a pioneer. It trails Stripe & Adyen in growth and innovation. Adyen is public and reported approximately 2x as much TPV at 20%+ growth rates. Stripe is likely growing at similar rates. PSP sustained its TPV share by undercutting market pricing, but has reversed that.

I think PayPal should divest this business. It still has an attractive client base, from inertia, but it doesn’t play a strategic role to “Win Checkout”. Price per transaction is low even if the margins are high. In other words, it adds more TPV than it does revenue or profit.

The unit has more value to an incumbent acquirer like a JPM, BAC, Fiserv, or GPN who can cross-sell the CNP service into their POS-centric clients. GPN has a similar business from Worldpay, but the others do not.

Transaction loss impact

This is a minor factor in results, but a positive trend. What isn’t clear is whether this is a performance improvement (i.e., better fraud detection) or a mix issue (more Debit). In-person debit has low fraud due to EMV. Lower fraud rates may be a side effect of debit growth unrelated to any PayPal investments.

This initiative is worthy, but not strategic. Every payments company tries to reduce fraud losses and PayPal doesn’t disclose anything unique.

Scale Next Gen Growth Vectors (Page 8)

This is a new “Driver” category with four named initiatives:

Advertising: I discussed this in this post, I am doubtful Advertising will be more than a modest contributor

Agentic: No one knows how big this will be – it is simply too early. PayPal would have gotten some of these transactions pre-agentic, so embedding in agents merely prevents attrition rather than grows TPV. The bet must be that more people will use wallets in agents than cards-on-file. The Networks beg to differ.

Stablecoins: PayPal has advantages here: They can pay rewards for SC usage and they can insert PYUSD into their $200B+ of cross-border TPV. It is unclear if this is happening, as they don’t mention anything about PYUSD in this report

PayPal World: This is another cross-border initiative to create a wallet-to-wallet network. PayPal would partners with local market leaders like Mercado Pago and UPI, but it isn’t clear how much TPV is at issue or how the economics work

PayPal World and PYUSD target the same $200B+ in cross-border flows, which are ~12% of PayPal’s 2025 TPV. It isn’t clear how the two initiatives divide this TPV or if PayPal instead expects incremental TPV.

All of these are properly labelled as “long-term”, so the lack of disclosure is fair. Of course, as long-term bets, they should be discounted as well.

What can PayPal do to “Win at Checkout” (Page 5)

This is PayPal’s existential challenge; everything else either needs to support this or be put aside. I first diagnose what went wrong, and then provide a suggested, and likely naïve, solution.

What went wrong

The core PayPal wallet just isn’t growing. They report virtually flat Active Accounts using the very forgiving definition of “active” as 1 transaction in 12 months. Monthly Actives (MAAs) are 52% of actives and grew 2% in 2025. Reported Actives and MAA include Venmo, which is growing faster, but adds mostly non-revenue-generating P2P transactions or marginally accretive debit transactions. Given the growth they report on Venmo, it is possible that core PayPal wallet accounts and transactions are shrinking.

I have written elsewhere how the market constrains PayPal wallet’s US share, but will re-summarize here:

Browser-based eCommerce. PayPal is the market leader but disadvantaged at key venues:

Amazon doesn’t accept it

Apple Store, Walmart.com, Shopify, Stripe & eBay favor their own solutions in their “territories”

Apple Pay, Paze & Google Pay (wallet and form-filler) compete for open space

Point of Sale. The wallet can’t be used in most stores and debit is both cumbersome and less profitable

In-app. Apple Pay dominates due to App Store rules and OS integration

Bill Pay, the wallet has some traction, but billers disfavor its high MDRs

Loan repayments (i.e., Card, Mortgage, Auto, etc.). None accept wallets; this category is about 50% of all bills

Other bills. The wallet is useable at some billers, but some of those are starting to steer to ACH to reduce acceptance costs

All this competition carves away growth opportunities. In other words, TAM is still enormous, SAM is much lower (i.e., ex-Amazon, POS, most bill pay, etc.), and SOM may be shrinking as the walled gardens (e.g., Shopify) favor their own solutions.

PayPal wallet never had high engagement even among its most active customers. Most users buy something with the wallet less than one time per month. Page 6 focuses on improved digital experience and marketing to drive adoption and engagement. These efforts haven’t yet inflected any metric. Sometimes, Digital Experience just isn’t the key to everything.

PayPal is no longer the lowest friction, safest payment option, but merely at parity. Other wallets are just as safe, with equivalent friction, and, often, better placement. This is why I believe the real problem is that the market moved against PayPal.

What can PayPal do about it

Friction and safety are commoditized, so PayPal needs a new differentiator. Getting to the POS may be possible when Apple opens its NFC chip, but that would not be differentiating. Further, any PayPal NFC implementation simply can’t be as friction-free as Apple Pay itself. In Android, where PayPal was never blocked, PayPal at the POS still didn’t break out. Finally, Apple will charge access fees for NFC, which would reduce PayPal margins. NFC might increase engagement for diehard users, but wouldn’t impact account acquisition, i.e., more transactions (good), but not more accounts (bad).

I think they started down the right path with Honey, but didn’t go far enough. Saving wallet users money is the only meaningful differentiator that might spur usage. To do that economically, PayPal needs to tap into CPG promotional spend, which in turn requires access to SKU. Today, PayPal rarely has SKU access.

The merchants might be incented to participate by lowering MDR if they provide SKU and position PayPal in the purchase path (like BNPL). Only redeemed offers might get the lower MDR, not all SKU sharing. In that model, the Merchant sees the direct benefit of sharing rather than relying on ambiguous conversion rates at checkout. The merchant would likely demand safeguards on how the SKU data is used, so the SKU data likely wouldn’t help PayPal’s advertising effort. The increase in wallet spend is what matters.

PayPal could require A2A funding methods to fund offer-incented purchases, recovering the cost of the MDR reductions via lower funding costs.

This might shift PayPal’s customer base somewhat down-market, to more budget conscious consumers. But savings opportunities would encourage those consumers to choose PayPal more often as their payment method. Being in the purchase path, would improve prospects for PayPal’s lending products as well.

Conclusions

It was easy for me to write this but would be very difficult for PayPal to pull off. Extremely difficult! They would have to recruit merchants and CPGs to participate, they would have to rewire their merchant experience to work pre-checkout, and they would have to re-structure their pricing to incent for SKU-sharing. They would have to carve-out Braintree and rethink the debit strategy. They would have to incent for A2A on “offers” transactions without aggravating the Networks. I could go on.

But the benefits are as clear as the heavy lifting involved: More accounts, higher engagement, more spending and more lending. Unless someone can suggest a better differentiator than “we save you money”, I’m not sure what other path they might pursue. The headwinds are not going away and there is no offsetting tailwind.